基于 VIX 指数的择时策略

波动率VIX指数是跟踪市场波动性的指数,一般通过标的期权的隐含波动率计算得来,以芝加哥期权交易所的VIX指数为例,如标的期权的隐含波动率越高,则VIX指数相应越高,一般而言,该指数反映出投资者愿意付出多少成本去对冲投资风险。业内认为,当VIX越高时,表示市场参与者预期后市波动程度会更加激烈,同时也反映其不安的心理状态;相反,VIX越低时,则反映市场参与者预期后市波动程度会趋于缓和的心态。因此,VIX又被称为投资人恐慌指标(The Investor Fear Gauge)。

中国波指是由上证所发布,用于衡量上证50ETF未来30日的预期波动。该指数是根据方差互换的原理,结合50ETF期权的实际运作特点,并通过对上证所交易的50ETF期权价格的计算编制而得。网址为:http://www.sse.com.cn/assortment/derivatives/options/volatility/

本文中,基于优矿平台,自己尝试计算了日间的中国波指,并将其用在了华夏上证50的择时买卖上,以验证VIX指数对未来的预测性

由于上证所未发布其iVIX计算方法,所以此处的计算基于CBOE发布的方法,具体参见:http://www.cboe.com/micro/vix/part2.aspx

策略思路

- 当VIX指数快速上升时,表示市场恐慌情绪蔓延,产生卖出信号

- 当VIX指数快速下降时,恐慌情绪有所舒缓,产生买入信号

- 卖出买入信号均用来买卖华夏上证50ETF基金

注:国内唯一一只期权上证50ETF期权,跟踪标的为华夏上证50ETF(510050)基金

1. 计算历史VIX指数

from matplotlibimport pylabimport numpyas npimport pandasas pdimport DataAPIimport seabornas snssns.set_style('white')from CAL.PyCALimport *from pandasimport Series, DataFrame, concatimport pandasas pdimport numpyas npimport seabornas snssns.set_style('white')from matplotlibimport pylabimport timeimport mathdefgetHistDayOptions(var, date):# 使用DataAPI.OptGet,拿到已退市和上市的所有期权的基本信息;# 同时使用DataAPI.MktOptdGet,拿到历史上某一天的期权成交信息;# 返回历史上指定日期交易的所有期权信息,包括:# optID varSecID contractType strikePrice expDate tradeDate closePrice# 以optID为index。 vixDateStr = date.toISO().replace('-','') optionsMkt = DataAPI.MktOptdGet(tradeDate = vixDateStr, field = [u"optID","tradeDate","closePrice"], pandas ="1") optionsMkt = optionsMkt.set_index(u"optID") optionsMkt.closePrice.name =u"price" optionsID = map(str, optionsMkt.index.values.tolist()) fieldNeeded = ["optID",u"varSecID",u'contractType',u'strikePrice',u'expDate'] optionsInfo = DataAPI.OptGet(optID=optionsID, contractStatus = [u"DE",u"L"], field=fieldNeeded, pandas="1") optionsInfo = optionsInfo.set_index(u"optID") options = concat([optionsInfo, optionsMkt], axis=1, join='inner').sort_index()return options[options.varSecID==var]defgetNearNextOptExpDate(options, vixDate):# 找到options中的当月和次月期权到期日;# 用这两个期权隐含的未来波动率来插值计算未来30隐含波动率,是为市场恐慌指数VIX;# 如果options中的最近到期期权离到期日仅剩1天以内,则抛弃这一期权,改# 选择次月期权和次月期权之后第一个到期的期权来计算。# 返回的near和next就是用来计算VIX的两个期权的到期日 optionsExpDate = Series(options.expDate.values.ravel()).unique().tolist() near = min(optionsExpDate) optionsExpDate.remove(near)if Date.parseISO(near) - vixDate <1: near = min(optionsExpDate) optionsExpDate.remove(near) next = min(optionsExpDate)return near, nextdefgetStrikeMinCallMinusPutClosePrice(options):# options 中包括计算某日VIX的call和put两种期权,# 对每个行权价,计算相应的call和put的价格差的绝对值,# 返回这一价格差的绝对值最小的那个行权价,# 并返回该行权价对应的call和put期权价格的差 call = options[options.contractType==u"CO"].set_index(u"strikePrice").sort_index() put = options[options.contractType==u"PO"].set_index(u"strikePrice").sort_index() callMinusPut = call.closePrice - put.closePrice strike = abs(callMinusPut).idxmin() priceDiff = callMinusPut[strike]return strike, priceDiffdefcalSigmaSquare(options, FF, R, T):# 计算某个到期日期权对于VIX的贡献sigma;# 输入为期权数据options,FF为forward index price,# R为无风险利率, T为期权剩余到期时间 callAll = options[options.contractType==u"CO"].set_index(u"strikePrice").sort_index() putAll = options[options.contractType==u"PO"].set_index(u"strikePrice").sort_index() callAll['deltaK'] =0.05 putAll['deltaK'] =0.05# Interval between strike prices index = callAll.indexif len(index) <3: callAll['deltaK'] = index[-1] - index[0]else:for iin range(1,len(index)-1): callAll['deltaK'].ix[index[i]] = (index[i+1]-index[i-1])/2.0 callAll['deltaK'].ix[index[0]] = index[1]-index[0] callAll['deltaK'].ix[index[-1]] = index[-1] - index[-2] index = putAll.indexif len(index) <3: putAll['deltaK'] = index[-1] - index[0]else:for iin range(1,len(index)-1): putAll['deltaK'].ix[index[i]] = (index[i+1]-index[i-1])/2.0 putAll['deltaK'].ix[index[0]] = index[1]-index[0] putAll['deltaK'].ix[index[-1]] = index[-1] - index[-2] call = callAll[callAll.index > FF] put = putAll[putAll.index < FF] FF_idx = FFifnot put.empty: FF_idx = put.index[-1] put['closePrice'].iloc[-1] = (putAll.ix[FF_idx].closePrice + callAll.ix[FF_idx].closePrice)/2.0 callComponent = call.closePrice*call.deltaK/call.index/call.index putComponent = put.closePrice*put.deltaK/put.index/put.index sigma = (sum(callComponent)+sum(putComponent))*np.exp(T*R)*2/T sigma = sigma - (FF/FF_idx -1)**2/Treturn sigmadefcalDayVIX(optionVarSecID, vixDate):# 利用CBOE的计算方法,计算历史某一日的未来30日期权波动率指数VIX# The risk-free interest rates R_near =0.06 R_next =0.06# 拿取所需期权信息 options = getHistDayOptions(optionVarSecID, vixDate) termNearNext = getNearNextOptExpDate(options, vixDate) optionsNearTerm = options[options.expDate == termNearNext[0]] optionsNextTerm = options[options.expDate == termNearNext[1]]# time to expiration T_near = (Date.parseISO(termNearNext[0]) - vixDate)/365.0 T_next = (Date.parseISO(termNearNext[1]) - vixDate)/365.0# the forward index prices nearPriceDiff = getStrikeMinCallMinusPutClosePrice(optionsNearTerm) nextPriceDiff = getStrikeMinCallMinusPutClosePrice(optionsNextTerm) near_F = nearPriceDiff[0] + np.exp(T_near*R_near)*nearPriceDiff[1] next_F = nextPriceDiff[0] + np.exp(T_next*R_next)*nextPriceDiff[1]# 计算不同到期日期权对于VIX的贡献 near_sigma = calSigmaSquare(optionsNearTerm, near_F, R_near, T_near) next_sigma = calSigmaSquare(optionsNextTerm, next_F, R_next, T_next)# 利用两个不同到期日的期权对VIX的贡献sig1和sig2,# 已经相应的期权剩余到期时间T1和T2;# 差值得到并返回VIX指数(%) w = (T_next -30.0/365.0)/(T_next - T_near) vix = T_near*w*near_sigma + T_next*(1 - w)*next_sigmareturn100*np.sqrt(vix*365.0/30.0)defgetHistVIX(beginDate, endDate):# 计算历史一段时间内的VIX指数并返回 optionVarSecID =u"510050.XSHG" cal = Calendar('China.SSE') dates = cal.bizDatesList(beginDate, endDate) dates = map(Date.toDateTime, dates) histVIX = pd.DataFrame(0.0, index=dates, columns=['VIX']) histVIX.index.name ='date'for datein histVIX.index: histVIX['VIX'][date] = calDayVIX(optionVarSecID, Date.fromDateTime(date))return histVIXdefgetDayVIX(date): optionVarSecID =u"510050.XSHG"return calDayVIX(optionVarSecID, date)2. VIX指数与华夏上证50ETF基金的走势对比

secID ='510050.XSHG'begin = Date(2015,2,9)end = Date(2015,7,23)# 历史VIXhistVIX = getHistVIX(begin, end)# 华夏上证50ETFetf = DataAPI.MktFunddGet(secID, beginDate=begin.toISO().replace('-',''), endDate=end.toISO().replace('-',''), field=['tradeDate','closePrice'])etf['tradeDate'] = pd.to_datetime(etf['tradeDate'])etf = etf.set_index('tradeDate')font.set_size(12)pylab.figure(figsize = (16,8))ax1 = histVIX.plot(x=histVIX.index, y='VIX', style='r')ax1.set_xlabel(u'日期', fontproperties=font)ax1.set_ylabel(u'VIX(%)', fontproperties=font)ax2 = ax1.twinx()ax2.plot(etf.index,etf.closePrice)ax2.set_ylabel(u'ETF Price', fontproperties=font)<matplotlib.text.Text at0x5a66390>

关于VIX,比较成熟的美国市场中,标普500指数和相应的VIX之间呈负相关性。具体可以参照CBOE的数据:http://www.cboe.com/micro/vix/part3.aspx

这可以理解为:

- 当VIX越高时,表示市场参与者预期后市波动程度会更加激烈,所以谨慎持仓,甚至逐渐减仓;

- 相反,VIX越低时,市场参与者预期后市波动程度会趋于缓和,开始放心投资股市。

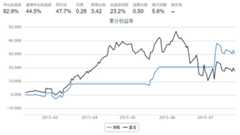

上图中的中国市场VIX指数与华夏上证50ETF走势对比中,我们不难发现以下几点:

- 上证50ETF期权于2月9日上市,之后一个月VIX稳定在低位运行,同时市场也表现出稳定的态势

- 3月下旬到5月初一段时间,VIX指数显著上升,表示市场认为后期震荡会加剧,但这种恐慌淹没在牛市大潮中

- 5月到6月VIX高位运行,但似乎没有引起市场的足够重视

- 6月中的股市大跌开始后,VIX指数快速上升到接近60

- 7月时候,市场认可国家救市决心,VIX开始从高位迅速下降,股指也日趋稳定

可以看出,VIX指数在和股指的并驾齐驱中总是慢人一步,没法充分表现出股指在六月极高位时候市场的不安;实际上,国内期权市场建立不足半年,期权流动性并不够大,导致基于期权市场的VIX指数对于中国股市的预测并不如成熟市场一样流畅

3. 基于VIX指数的择时策略示例

start = datetime(2015,2,9)# 回测起始时间end = datetime(2015,7,26)# 回测结束时间benchmark ='510050.XSHG'# 策略参考标准universe = ['510050.XSHG']# 股票池capital_base =100000# 起始资金commission = Commission(0.0,0.0)window_short =1window_long =5longest_history =1SD =0.08histVIX['short_window'] = pd.rolling_mean(histVIX['VIX'], window=window_short)histVIX['long_window'] = pd.rolling_mean(histVIX['VIX'], window=window_long)definitialize(account):# 初始化虚拟账户状态 account.fund = universe[0]defhandle_data(account):# 每个交易日的买入卖出指令 hist = account.get_history(longest_history) fund = account.fund# 获取回测当日的前一天日期 dt = Date.fromDateTime(account.current_date) cal = Calendar('China.IB') lastTDay = cal.advanceDate(dt,'-1B',BizDayConvention.Preceding)#计算出前一个交易日期 last_day_str = lastTDay.strftime("%Y-%m-%d")# 计算买入卖出信号try: short_mean = histVIX['short_window'].loc[last_day_str]# 计算短均线值 long_mean = histVIX['long_window'].loc[last_day_str]# 计算长均线值 long_flag =Trueif (short_mean - long_mean) < -SD * long_meanelseFalse short_flag =Trueif (short_mean - long_mean) > SD * long_meanelseFalseexcept: long_flag =False short_flag =Falseif long_flag:if account.position.secpos.get(fund,0) ==0:# 空仓时全仓买入,买入股数为100的整数倍 approximationAmount = int(account.cash / hist[fund]['closePrice'][-1]/100.0) *100 order(fund, approximationAmount)elif short_flag:# 卖出时,全仓清空if account.position.secpos.get(fund,0) >=0: order_to(fund,0)

可以看出:

- 基于VIX指数高位时空仓、低位时进场的策略,可以比较有效地避开股指大跌的风险

- 但由于国内期权市场流动性不足,VIX指数并不能有效反应市场的情绪,导致我们也错过了很多牛市的蛋糕