KR20230106533A - Method and application for easy payment in mart - Google Patents

Method and application for easy payment in martDownload PDFInfo

- Publication number

- KR20230106533A KR20230106533AKR1020230068756AKR20230068756AKR20230106533AKR 20230106533 AKR20230106533 AKR 20230106533AKR 1020230068756 AKR1020230068756 AKR 1020230068756AKR 20230068756 AKR20230068756 AKR 20230068756AKR 20230106533 AKR20230106533 AKR 20230106533A

- Authority

- KR

- South Korea

- Prior art keywords

- terminal

- payment

- information

- payment device

- screen

- Prior art date

- Legal status (The legal status is an assumption and is not a legal conclusion. Google has not performed a legal analysis and makes no representation as to the accuracy of the status listed.)

- Pending

Links

Images

Classifications

- G—PHYSICS

- G06—COMPUTING OR CALCULATING; COUNTING

- G06Q—INFORMATION AND COMMUNICATION TECHNOLOGY [ICT] SPECIALLY ADAPTED FOR ADMINISTRATIVE, COMMERCIAL, FINANCIAL, MANAGERIAL OR SUPERVISORY PURPOSES; SYSTEMS OR METHODS SPECIALLY ADAPTED FOR ADMINISTRATIVE, COMMERCIAL, FINANCIAL, MANAGERIAL OR SUPERVISORY PURPOSES, NOT OTHERWISE PROVIDED FOR

- G06Q20/00—Payment architectures, schemes or protocols

- G06Q20/30—Payment architectures, schemes or protocols characterised by the use of specific devices or networks

- G06Q20/32—Payment architectures, schemes or protocols characterised by the use of specific devices or networks using wireless devices

- G06Q20/326—Payment applications installed on the mobile devices

- G—PHYSICS

- G06—COMPUTING OR CALCULATING; COUNTING

- G06Q—INFORMATION AND COMMUNICATION TECHNOLOGY [ICT] SPECIALLY ADAPTED FOR ADMINISTRATIVE, COMMERCIAL, FINANCIAL, MANAGERIAL OR SUPERVISORY PURPOSES; SYSTEMS OR METHODS SPECIALLY ADAPTED FOR ADMINISTRATIVE, COMMERCIAL, FINANCIAL, MANAGERIAL OR SUPERVISORY PURPOSES, NOT OTHERWISE PROVIDED FOR

- G06Q20/00—Payment architectures, schemes or protocols

- G06Q20/04—Payment circuits

- G06Q20/047—Payment circuits using payment protocols involving electronic receipts

- G—PHYSICS

- G06—COMPUTING OR CALCULATING; COUNTING

- G06Q—INFORMATION AND COMMUNICATION TECHNOLOGY [ICT] SPECIALLY ADAPTED FOR ADMINISTRATIVE, COMMERCIAL, FINANCIAL, MANAGERIAL OR SUPERVISORY PURPOSES; SYSTEMS OR METHODS SPECIALLY ADAPTED FOR ADMINISTRATIVE, COMMERCIAL, FINANCIAL, MANAGERIAL OR SUPERVISORY PURPOSES, NOT OTHERWISE PROVIDED FOR

- G06Q20/00—Payment architectures, schemes or protocols

- G06Q20/08—Payment architectures

- G06Q20/14—Payment architectures specially adapted for billing systems

- G—PHYSICS

- G06—COMPUTING OR CALCULATING; COUNTING

- G06Q—INFORMATION AND COMMUNICATION TECHNOLOGY [ICT] SPECIALLY ADAPTED FOR ADMINISTRATIVE, COMMERCIAL, FINANCIAL, MANAGERIAL OR SUPERVISORY PURPOSES; SYSTEMS OR METHODS SPECIALLY ADAPTED FOR ADMINISTRATIVE, COMMERCIAL, FINANCIAL, MANAGERIAL OR SUPERVISORY PURPOSES, NOT OTHERWISE PROVIDED FOR

- G06Q20/00—Payment architectures, schemes or protocols

- G06Q20/08—Payment architectures

- G06Q20/14—Payment architectures specially adapted for billing systems

- G06Q20/145—Payments according to the detected use or quantity

- G—PHYSICS

- G06—COMPUTING OR CALCULATING; COUNTING

- G06Q—INFORMATION AND COMMUNICATION TECHNOLOGY [ICT] SPECIALLY ADAPTED FOR ADMINISTRATIVE, COMMERCIAL, FINANCIAL, MANAGERIAL OR SUPERVISORY PURPOSES; SYSTEMS OR METHODS SPECIALLY ADAPTED FOR ADMINISTRATIVE, COMMERCIAL, FINANCIAL, MANAGERIAL OR SUPERVISORY PURPOSES, NOT OTHERWISE PROVIDED FOR

- G06Q20/00—Payment architectures, schemes or protocols

- G06Q20/08—Payment architectures

- G06Q20/16—Payments settled via telecommunication systems

- G—PHYSICS

- G06—COMPUTING OR CALCULATING; COUNTING

- G06Q—INFORMATION AND COMMUNICATION TECHNOLOGY [ICT] SPECIALLY ADAPTED FOR ADMINISTRATIVE, COMMERCIAL, FINANCIAL, MANAGERIAL OR SUPERVISORY PURPOSES; SYSTEMS OR METHODS SPECIALLY ADAPTED FOR ADMINISTRATIVE, COMMERCIAL, FINANCIAL, MANAGERIAL OR SUPERVISORY PURPOSES, NOT OTHERWISE PROVIDED FOR

- G06Q20/00—Payment architectures, schemes or protocols

- G06Q20/30—Payment architectures, schemes or protocols characterised by the use of specific devices or networks

- G06Q20/32—Payment architectures, schemes or protocols characterised by the use of specific devices or networks using wireless devices

- G06Q20/327—Short range or proximity payments by means of M-devices

- G06Q20/3278—RFID or NFC payments by means of M-devices

- G—PHYSICS

- G06—COMPUTING OR CALCULATING; COUNTING

- G06Q—INFORMATION AND COMMUNICATION TECHNOLOGY [ICT] SPECIALLY ADAPTED FOR ADMINISTRATIVE, COMMERCIAL, FINANCIAL, MANAGERIAL OR SUPERVISORY PURPOSES; SYSTEMS OR METHODS SPECIALLY ADAPTED FOR ADMINISTRATIVE, COMMERCIAL, FINANCIAL, MANAGERIAL OR SUPERVISORY PURPOSES, NOT OTHERWISE PROVIDED FOR

- G06Q20/00—Payment architectures, schemes or protocols

- G06Q20/38—Payment protocols; Details thereof

- G06Q20/382—Payment protocols; Details thereof insuring higher security of transaction

- G—PHYSICS

- G06—COMPUTING OR CALCULATING; COUNTING

- G06Q—INFORMATION AND COMMUNICATION TECHNOLOGY [ICT] SPECIALLY ADAPTED FOR ADMINISTRATIVE, COMMERCIAL, FINANCIAL, MANAGERIAL OR SUPERVISORY PURPOSES; SYSTEMS OR METHODS SPECIALLY ADAPTED FOR ADMINISTRATIVE, COMMERCIAL, FINANCIAL, MANAGERIAL OR SUPERVISORY PURPOSES, NOT OTHERWISE PROVIDED FOR

- G06Q20/00—Payment architectures, schemes or protocols

- G06Q20/38—Payment protocols; Details thereof

- G06Q20/387—Payment using discounts or coupons

- G—PHYSICS

- G06—COMPUTING OR CALCULATING; COUNTING

- G06Q—INFORMATION AND COMMUNICATION TECHNOLOGY [ICT] SPECIALLY ADAPTED FOR ADMINISTRATIVE, COMMERCIAL, FINANCIAL, MANAGERIAL OR SUPERVISORY PURPOSES; SYSTEMS OR METHODS SPECIALLY ADAPTED FOR ADMINISTRATIVE, COMMERCIAL, FINANCIAL, MANAGERIAL OR SUPERVISORY PURPOSES, NOT OTHERWISE PROVIDED FOR

- G06Q20/00—Payment architectures, schemes or protocols

- G06Q20/38—Payment protocols; Details thereof

- G06Q20/40—Authorisation, e.g. identification of payer or payee, verification of customer or shop credentials; Review and approval of payers, e.g. check credit lines or negative lists

- G06Q20/401—Transaction verification

- G—PHYSICS

- G06—COMPUTING OR CALCULATING; COUNTING

- G06Q—INFORMATION AND COMMUNICATION TECHNOLOGY [ICT] SPECIALLY ADAPTED FOR ADMINISTRATIVE, COMMERCIAL, FINANCIAL, MANAGERIAL OR SUPERVISORY PURPOSES; SYSTEMS OR METHODS SPECIALLY ADAPTED FOR ADMINISTRATIVE, COMMERCIAL, FINANCIAL, MANAGERIAL OR SUPERVISORY PURPOSES, NOT OTHERWISE PROVIDED FOR

- G06Q20/00—Payment architectures, schemes or protocols

- G06Q20/38—Payment protocols; Details thereof

- G06Q20/40—Authorisation, e.g. identification of payer or payee, verification of customer or shop credentials; Review and approval of payers, e.g. check credit lines or negative lists

- G06Q20/401—Transaction verification

- G06Q20/4012—Verifying personal identification numbers [PIN]

- G—PHYSICS

- G06—COMPUTING OR CALCULATING; COUNTING

- G06Q—INFORMATION AND COMMUNICATION TECHNOLOGY [ICT] SPECIALLY ADAPTED FOR ADMINISTRATIVE, COMMERCIAL, FINANCIAL, MANAGERIAL OR SUPERVISORY PURPOSES; SYSTEMS OR METHODS SPECIALLY ADAPTED FOR ADMINISTRATIVE, COMMERCIAL, FINANCIAL, MANAGERIAL OR SUPERVISORY PURPOSES, NOT OTHERWISE PROVIDED FOR

- G06Q20/00—Payment architectures, schemes or protocols

- G06Q20/38—Payment protocols; Details thereof

- G06Q20/40—Authorisation, e.g. identification of payer or payee, verification of customer or shop credentials; Review and approval of payers, e.g. check credit lines or negative lists

- G06Q20/401—Transaction verification

- G06Q20/4014—Identity check for transactions

- G06Q20/40145—Biometric identity checks

- G—PHYSICS

- G08—SIGNALLING

- G08B—SIGNALLING OR CALLING SYSTEMS; ORDER TELEGRAPHS; ALARM SYSTEMS

- G08B3/00—Audible signalling systems; Audible personal calling systems

- G08B3/10—Audible signalling systems; Audible personal calling systems using electric transmission; using electromagnetic transmission

- G—PHYSICS

- G08—SIGNALLING

- G08B—SIGNALLING OR CALLING SYSTEMS; ORDER TELEGRAPHS; ALARM SYSTEMS

- G08B6/00—Tactile signalling systems, e.g. personal calling systems

Landscapes

- Business, Economics & Management (AREA)

- Accounting & Taxation (AREA)

- Engineering & Computer Science (AREA)

- Physics & Mathematics (AREA)

- General Physics & Mathematics (AREA)

- General Business, Economics & Management (AREA)

- Strategic Management (AREA)

- Theoretical Computer Science (AREA)

- Finance (AREA)

- Computer Security & Cryptography (AREA)

- Computer Networks & Wireless Communication (AREA)

- Development Economics (AREA)

- Economics (AREA)

- Electromagnetism (AREA)

- Financial Or Insurance-Related Operations Such As Payment And Settlement (AREA)

Abstract

Description

Translated fromKorean본 개시는 마트 혹은 백화점 혹은 소형 가게 등등의 다양한 장소에서 물품이나 서비스를 거래할 때 결제를 수행하는 방법 및 어플리케이션에 관한 것으로, 현장에서 스마트폰 등의 단말로 결제를 수행할 때 스마트폰을 꺼진 화면 상태 혹은 잠금 화면 상태에서도 편리하게 결제를 수행하는 방법 및 어플리케이션에 관한 것이다.The present disclosure relates to a method and application for performing payment when trading goods or services in various places such as a mart, department store, or small shop, etc. It relates to a method and application for conveniently performing payment even in a state or lock screen state.

스마트폰을 이용한 간편결제 방식에는 대표적으로 삼성페이와 애플페이가 있다. 삼성페이는 카드 정보를 마그네틱 보안 전송(magnetic secure transmission, MST)을 이용하여 결제 기기에 전송하는 방식이고, 애플페이는 카드 정보를 비접촉 근거리 통신(near field communication, NFC)을 이용하여 전송한다. 상술된 페이를 위하여 스마트폰에서 사용자 보안 인증이 수행되는데, 일반적으로 비밀번호 입력 혹은 홍채인식, 안면인식, 지문 등의 생체인식 방식들이 많이 사용된다.Simple payment methods using smartphones include Samsung Pay and Apple Pay. Samsung Pay transmits card information to a payment device using magnetic secure transmission (MST), and Apple Pay transmits card information using near field communication (NFC). User security authentication is performed on a smartphone for the above-described pay, and in general, biometric methods such as password input or iris recognition, face recognition, and fingerprints are widely used.

한편, 카드 단말기와 스마트폰은 근거리 무선통신으로 연결되는데, 이러한 근거리 무선통신에는 블루투스(bluetooth), NFC, MST가 있으며, 2021년부터 삼성과 애플의 스마트폰 제품들 중의 일부는 초광대역(ultra-wideband, UWB) 통신을 제공하기도 한다. 이외에도 근거리에서 사용이 가능한 단말간 통신은 여러 가지가 존재하며, 예를 들면 와이파이 다이렉트(wifi-direct) 등이 있다. 이와 같이 단말간 직접 정보 교환이 가능한 무선 통신을 단말간(device to device, D2D) 통신이라고 부른다.On the other hand, the card terminal and the smartphone are connected by short-range wireless communication. Such short-range wireless communication includes Bluetooth, NFC, and MST. It also provides wideband (UWB) communications. In addition, there are several types of terminal-to-device communication that can be used in a short distance, for example, Wi-Fi-direct. In this way, wireless communication capable of direct information exchange between terminals is called device to device (D2D) communication.

그런데, 위 두가지 페이 방식은 모두 단말이 꺼짐 화면 상태이거나 잠금 화면 상태에서 사용자가 결제를 수행하지 못하는 불편함이 있다.However, both of the above two payment methods have inconvenience in that the user cannot perform payment when the terminal is in a screen off state or in a lock screen state.

상기와 같은 문제점을 해결하기 위한 본 개시의 목적은, 사람들이 마트 혹은 백화점 혹은 소형 가게 등등의 다양한 장소에서 물품이나 서비스를 거래할 때, 사용자가 스마트폰이 꺼진 화면 상태에서 혹은 잠금 화면 상태에서도 편리하게 결제를 수행할 수 있는 방법 및 어플리케이션을 제공하는 데 있다.An object of the present disclosure to solve the above problems is that when people trade goods or services in various places such as marts, department stores, or small shops, the user can conveniently use the smartphone in a turned off screen state or in a locked screen state. It is to provide a method and an application capable of performing a payment in an easy way.

본 발명에서 이루고자 하는 기술적 과제는 이상에서 언급한 기술적 과제로 제한되지 않으며, 언급하지 않은 또 다른 기술적 과제들은 아래의 기재로부터 본 발명이 속하는 기술분야에서 통상의 지식을 가진 자에게 명확하게 이해될 수 있을 것이다.The technical problem to be achieved in the present invention is not limited to the above-mentioned technical problem, and other technical problems not mentioned can be clearly understood by those skilled in the art from the description below. There will be.

상기 목적을 달성하기 위한 본 개시의 일 실시예에 따른 간편페이 어플리케이션이 설치된 제1 단말의 동작 방법은,In order to achieve the above object, a method of operating a first terminal in which a simple pay application is installed according to an embodiment of the present disclosure,

꺼짐 화면 혹은 잠금 화면 상태에서 단말간 통신을 이용하여 결제장치를 인식하는 단계; 상기 결제장치와 결제 준비 정보를 무선으로 주고받는 단계; 제1 단말의 화면에 상기 결제 정보가 표시되는 단계; 사용자로부터 사용자 인증 정보를 입력받는 단계; 및 상기 결제장치에게 상기 결제의 실행 정보를 전송하는 단계를 포함할 수 있다.Recognizing a payment device using device-to-device communication in an off-screen or lock-screen state; wirelessly exchanging payment preparation information with the payment device; displaying the payment information on a screen of a first terminal; Receiving user authentication information from a user; and transmitting execution information of the payment to the payment device.

본 발명의 일 실시예에서, 제1 단말이 상기 결제장치를 인식하기 위하여 사용하는 단말간 통신은 블루투스, NFC, MST, UWB, wifi-direct 중의 하나일 수 있다.In one embodiment of the present invention, communication between terminals used by the first terminal to recognize the payment device may be one of Bluetooth, NFC, MST, UWB, and wifi-direct.

본 발명의 일 실시예에서, 상기 결제장치를 단말간 통신을 이용하여 인식하는 방법은, 제1 단말이 상기 결제장치가 단말간 통신을 이용하여 방송하는 결제장치 인식 정보를 수신하는 것일 수 있다.In one embodiment of the present invention, the method of recognizing the payment device using terminal-to-device communication may be that the first terminal receives payment device recognition information broadcasted by the payment device using terminal-to-device communication.

본 발명의 일 실시예에서, 제1 단말이 상기 결제장치를 단말간 통신을 이용하여 인식하기 위한 조건은, 제1 단말이 상기 결제장치에 미리 정한 임계 거리 이내로 근접하거나 혹은 제1 단말에서 상기 결제장치가 전송하는 무선 신호의 수신 파워가 미리 정한 임계 파워보다 높거나 혹은 제1 단말의 단말간 통신 장치가 상기 결제장치가 전송하는 신호에 의하여 활성화되는 것일 수 있다.In one embodiment of the present invention, the condition for the first terminal to recognize the payment device using terminal-to-device communication is that the first terminal approaches the payment device within a predetermined threshold distance or the first terminal makes the payment. The reception power of the radio signal transmitted by the device may be higher than a predetermined threshold power, or the terminal-to-device communication device of the first terminal may be activated by the signal transmitted by the payment device.

본 발명의 일 실시예에서, 제1 단말이 상기 결제장치를 단말간 통신을 이용하여 인식하는 방법은, 상기 결제장치로부터 결제 대상임을 통보받는 것일 수 있다.In one embodiment of the present invention, a method for the first terminal to recognize the payment device using terminal-to-terminal communication may be to receive a notification that the payment device is a payment target.

여기서, 제1 단말이 상기 결제장치로부터 결제 대상임을 통보받는 방법은, 상기 결제장치가 상기 결제장치로부터 가장 거리가 가까운 단말로 제1 단말을 선택하여 제1 단말에게 결제 대상임을 통지하는 단말간 통신 신호를 수신하거나, 혹은 상기 결제장치가 단말간 통신 신호의 수신 파워가 가장 큰 단말로 제1 단말을 선택하여 제1 단말에게 결제 대상임을 통지하는 단말간 통신 신호를 수신하는 것일 수 있다.Here, the method for the first terminal to be notified that the payment device is subject to payment includes terminal-to-device communication in which the payment device selects the first terminal as a terminal closest to the payment device and notifies the first terminal that the first terminal is subject to payment. A signal may be received, or the payment device may select the first terminal as a terminal having the highest reception power of the inter-device communication signal and receive a terminal-to-device communication signal notifying the first terminal that the first terminal is subject to payment.

본 발명의 일 실시예에서, 상기 결제장치와 무선으로 주고받는 결제 준비 정보는, 가게 이름, 결제할 금액, 할부 정보, 적립포인트 중의 결제 가능한 금액, 사용 가능한 할인 쿠폰, 사용자 개인 정보 중의 하나 이상을 포함할 수 있다.In one embodiment of the present invention, the payment preparation information wirelessly exchanged with the payment device includes one or more of a shop name, an amount to be paid, installment information, a payable amount among accumulated points, available discount coupons, and user personal information. can include

본 발명의 일 실시예에서, 단말의 화면에 표시되는 상기 결제 정보는 가게 이름, 결제할 금액, 결제할 카드 이름, 할부 정보, 적립포인트 중의 결제 가능한 금액, 사용 가능한 할인 쿠폰 중의 하나 이상을 포함할 수 있다.In one embodiment of the present invention, the payment information displayed on the screen of the terminal may include one or more of the store name, amount to be paid, name of card to be paid, installment information, payment amount among accumulated points, and available discount coupons. can

본 발명의 일 실시예에서, 제1 단말의 화면에 상기 결제 정보가 표시되는 방법은, 꺼짐 화면 혹은 잠금 화면 상태에서 팝업으로 표시되는 것일 수 있다.In one embodiment of the present invention, the method of displaying the payment information on the screen of the first terminal may be displayed as a pop-up in a screen off or lock screen state.

본 발명의 일 실시예에서, 제1 단말이 사용자로부터 사용자 인증 정보를 입력받는 방법은, 지문 인식, 안면 인식, 패턴 인식, 비밀번호 입력 중의 하나 이상을 포함할 수 있다.In one embodiment of the present invention, the method for the first terminal to receive user authentication information from the user may include at least one of fingerprint recognition, face recognition, pattern recognition, and password input.

본 발명의 일 실시예에서, 상기 결제장치를 인식하고 상기 결제장치와 결제 준비 정보를 무선으로 주고받을 때 사용자 인증이 제1 단말에서 수행되는 경우, 제1 단말은 사용자로부터 사용자 인증 정보를 입력받는 단계를 생략할 수 있다.In one embodiment of the present invention, when user authentication is performed in the first terminal when recognizing the payment device and wirelessly exchanging payment preparation information with the payment device, the first terminal receives user authentication information from the user. step can be omitted.

본 발명의 일 실시예에서, 상기 결제장치를 인식하고 상기 결제장치와 결제 준비 정보를 무선으로 주고받을 때 사용자 인증이 제1 단말에서 수행되는 경우, 제1 단말은 제1 단말의 화면에 상기 결제 정보가 표시되는 단계와 사용자로부터 사용자 인증 정보를 입력받는 단계를 동시에 생략할 수 있다.In one embodiment of the present invention, when user authentication is performed in the first terminal when recognizing the payment device and wirelessly exchanging payment preparation information with the payment device, the first terminal displays the payment on the screen of the first terminal. The step of displaying information and the step of receiving user authentication information from the user may be simultaneously omitted.

본 발명의 일 실시예에서, 상기 결제장치를 인식하고 상기 결제장치와 결제 준비 정보를 무선으로 주고받을 때 사용자 인증이 제1 단말에서 수행되는 경우, 그 인증 수단이 지문이면, 제1 단말은 상기 인증에 사용된 지문과 미리 매핑(mapping)된 결제 수단을 상기 결제에 사용할 수 있다.In one embodiment of the present invention, when user authentication is performed in the first terminal when recognizing the payment device and wirelessly exchanging payment preparation information with the payment device, if the authentication means is a fingerprint, the first terminal A payment method pre-mapped with a fingerprint used for authentication may be used for the payment.

본 발명의 일 실시예에서, 꺼짐 화면 혹은 잠금 화면 상태에서 단말간 통신을 이용하여 결제장치를 인식하는 단계 이후에, 인식 알림음을 송출하거나 알림 진동을 수행하는 단계를 더 포함할 수 있다.In one embodiment of the present invention, after the step of recognizing the payment device using device-to-device communication in the off screen or lock screen state, the step of transmitting a recognition notification sound or performing a notification vibration may be further included.

본 발명의 일 실시예에서, 상기 결제장치에게 상기 결제의 실행 정보를 전송하는 단계 이후에, 제1 단말이 상기 결제장치로부터 상기 결제에 대한 승인 완료 정보를 수신하여, 상기 수신한 정보를 제1 단말의 화면에 표시하는 단계를 더 포함할 수 있다.In one embodiment of the present invention, after the step of transmitting the payment execution information to the payment device, the first terminal receives approval completion information for the payment from the payment device, and transmits the received information to the first terminal. The step of displaying on the screen of the terminal may be further included.

본 발명의 일 실시예에서, 상기 결제장치에게 상기 결제의 실행 정보를 전송하는 단계 이후에, 상기 결제장치로부터 상기 결제에 대한 영수증을 수신하여, 상기 수신한 영수증을 제1 단말의 화면에 표시하는 단계를 더 포함할 수 있다.In one embodiment of the present invention, after the step of transmitting the payment execution information to the payment device, receiving a receipt for the payment from the payment device, and displaying the received receipt on the screen of the first terminal Further steps may be included.

여기서, 상기 결제장치로부터 상기 결제에 대한 영수증을 수신하는 단계 이후에, 상기 수신한 결제 영수증을 상기 결제장치의 화면에 표시하기 위하여 상기 결제장치에게 송신하는 단계를 더 포함할 수 있다.Here, after receiving the payment receipt from the payment device, the method may further include transmitting the received payment receipt to the payment device to display on the screen of the payment device.

본 개시에 의하면, 사용자는 스마트폰 등의 단말로 결제를 수행할 때, 스마트폰의 화면이 꺼진 상태나 잠금 상태에 있더라도 편리하게 결제를 수행할 수 있다. 특히, 스마트폰 사용자가 지문 인증 등을 실시간으로 수행하는 경우, 단지 스마트폰을 결제기 근처에 가져가는 동작만으로도 결제를 완료할 수 있다.According to the present disclosure, when a user makes a payment with a terminal such as a smartphone, the user can conveniently perform the payment even if the screen of the smartphone is turned off or locked. In particular, when a smartphone user performs fingerprint authentication in real time, payment can be completed simply by bringing the smartphone near the payment machine.

본 발명에서 얻을 수 있는 효과는 이상에서 언급한 효과들로 제한되지 않으며, 언급하지 않은 또 다른 효과들은 아래의 기재로부터 본 발명이 속하는 기술분야에서 통상의 지식을 가진 자에게 명확하게 이해될 수 있을 것이다.The effects obtainable in the present invention are not limited to the effects mentioned above, and other effects not mentioned can be clearly understood by those skilled in the art from the description below. will be.

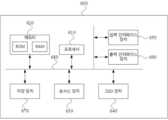

도 1은 본 발명의 일 실시예에 따른, 간편페이 결제 동작에 필요한 시스템 구성도이다.

도 2은 기존의 삼성페이가 동작하는 절차도이다.

도 3는 기존의 애플페이가 동작하는 절차도이다.

도 4는 본 발명의 일 실시예에 따른, 간편페이의 동작 흐름도이다.

도 5은 본 발명의 일 실시예에 따른, 간편페이의 확장 동작 흐름도이다.

도 6은 본 발명의 일 실시예에 따른, 간편페이에 사용되는 단말의 블록도이다.

1 is a system configuration diagram necessary for a simple pay payment operation according to an embodiment of the present invention.

2 is a flowchart illustrating the operation of existing Samsung Pay.

3 is a flowchart illustrating the operation of existing Apple Pay.

4 is an operation flow chart of Simple Pay according to an embodiment of the present invention.

5 is a flowchart of an expansion operation of a simple pay according to an embodiment of the present invention.

6 is a block diagram of a terminal used for simple pay according to an embodiment of the present invention.

본 개시는 다양한 변경을 가할 수 있고 여러 가지 실시예를 가질 수 있는 바, 특정 실시예들을 도면에 예시하고 상세하게 설명하고자 한다. 그러나, 이는 본 개시를 특정한 실시 형태에 대해 한정하려는 것이 아니며, 본 개시의 사상 및 기술 범위에 포함되는 모든 변경, 균등물 내지 대체물을 포함하는 것으로 이해되어야 한다.Since the present disclosure can make various changes and have various embodiments, specific embodiments are illustrated in the drawings and described in detail. However, this is not intended to limit the present disclosure to specific embodiments, and should be understood to include all modifications, equivalents, and substitutes included in the spirit and scope of the present disclosure.

본 개시의 실시예들에서, “A 및 B 중에서 적어도 하나”는 “A 또는 B 중에서 적어도 하나” 또는 “A 및 B 중 하나 이상의 조합들 중에서 적어도 하나”를 의미할 수 있다. 또한, 본 개시의 실시예들에서, “A 및 B 중에서 하나 이상”은 “A 또는 B 중에서 하나 이상” 또는 “A 및 B 중 하나 이상의 조합들 중에서 하나 이상”을 의미할 수 있다.In embodiments of the present disclosure, “at least one of A and B” may mean “at least one of A or B” or “at least one of combinations of one or more of A and B”. Also, in embodiments of the present disclosure, “one or more of A and B” may mean “one or more of A or B” or “one or more of combinations of one or more of A and B”.

어떤 구성요소가 다른 구성요소에 "연결되어" 있다거나 "접속되어" 있다고 언급된 때에는, 그 다른 구성요소에 직접적으로 연결되어 있거나 또는 접속되어 있을 수도 있지만, 중간에 다른 구성요소가 존재할 수도 있다고 이해되어야 할 것이다. 반면에, 어떤 구성요소가 다른 구성요소에 "직접 연결되어" 있다거나 "직접 접속되어" 있다고 언급된 때에는, 중간에 다른 구성요소가 존재하지 않는 것으로 이해되어야 할 것이다.It is understood that when an element is referred to as being "connected" or "connected" to another element, it may be directly connected or connected to the other element, but other elements may exist in the middle. It should be. On the other hand, when an element is referred to as “directly connected” or “directly connected” to another element, it should be understood that no other element exists in the middle.

본 개시에서 사용한 용어는 단지 특정한 실시예를 설명하기 위해 사용된 것으로, 본 개시를 한정하려는 의도가 아니다. 단수의 표현은 문맥상 명백하게 다르게 뜻하지 않는 한, 복수의 표현을 포함한다. 본 개시에서, "포함하다" 또는 "가지다" 등의 용어는 명세서상에 기재된 특징, 숫자, 단계, 동작, 구성요소, 부품 또는 이들을 조합한 것이 존재함을 지정하려는 것이지, 하나 또는 그 이상의 다른 특징들이나 숫자, 단계, 동작, 구성요소, 부품 또는 이들을 조합한 것들의 존재 또는 부가 가능성을 미리 배제하지 않는 것으로 이해되어야 한다.Terms used in the present disclosure are only used to describe specific embodiments, and are not intended to limit the present disclosure. Singular expressions include plural expressions unless the context clearly dictates otherwise. In the present disclosure, terms such as "comprise" or "having" are intended to indicate that there is a feature, number, step, operation, component, part, or combination thereof described in the specification, but one or more other features It should be understood that the presence or addition of numbers, steps, operations, components, parts, or combinations thereof is not precluded.

다르게 정의되지 않는 한, 기술적이거나 과학적인 용어를 포함해서 여기서 사용되는 모든 용어들은 본 개시가 속하는 기술 분야에서 통상의 지식을 가진 자에 의해 일반적으로 이해되는 것과 동일한 의미를 가지고 있다. 일반적으로 사용되는 사전에 정의되어 있는 것과 같은 용어들은 관련 기술의 문맥 상 가지는 의미와 일치하는 의미를 가진 것으로 해석되어야 하며, 본 개시에서 명백하게 정의하지 않는 한, 이상적이거나 과도하게 형식적인 의미로 해석되지 않는다.Unless defined otherwise, all terms used herein, including technical or scientific terms, have the same meaning as commonly understood by one of ordinary skill in the art to which this disclosure belongs. Terms such as those defined in commonly used dictionaries should be interpreted as having a meaning consistent with the meaning in the context of the related art, and unless explicitly defined in the present disclosure, they should not be interpreted in an ideal or excessively formal meaning. don't

본 개시에 따른 실시예들이 적용되는 결제 방법이 설명될 것이다. 본 개시에 따른 실시예들이 적용되는 결제 방법은 아래 설명된 내용에 한정되지 않으며, 본 개시에 따른 실시예들은 다양한 결제시스템에 적용될 수 있다.A payment method to which embodiments according to the present disclosure are applied will be described. Payment methods to which embodiments according to the present disclosure are applied are not limited to those described below, and embodiments according to the present disclosure may be applied to various payment systems.

명세서 전체에서 단말은 컴퓨터 판독 가능한 저장 매체에 저장되는 소프트웨어인 어플리케이션/프로그램, 그리고 프로세서, 메모리, 디스플레이, 통신 모듈 등의 하드웨어를 포함한다. 프로세서는 하드웨어들과 협력하여 어플리케이션을 구동한다. 디스플레이는 어플리케이션에서 제공하는 사용자 인터페이스 화면을 표시할 수 있다. 단말 종류에 따라서, 디스플레이는 사용자 입력을 수신할 수 있고, 예를 들면 터치 입력을 수신할 수 있다. 통신 모듈은 단말 간 직접(device to device, D2D) 통신을 포함할 수 있다. 또한, 단말은 통신망을 통해 서버와 통신할 수 있는 통신 모듈을 포함할 수 있다. 단말은 다양한 형태로 구현될 수 있는데, 통신이 가능한 태블릿(tablet) PC, 무선전화기(wireless phone), 모바일 폰(mobile phone), 스마트 폰(smart phone), 스마트 워치(smart watch), 스마트 글래스(smart glass), e-book 리더기, PMP(portable multimedia player), 휴대용 게임기, 네비게이션(navigation) 장치, 디지털 카메라(digital camera), DMB(digital multimedia broadcasting) 재생기, 디지털 음성 녹음기(digital audio recorder), 디지털 음성 재생기(digital audio player), 디지털 영상 녹화기(digital picture recorder), 디지털 동영상 재생기(digital picture player), 디지털 동영상 재생기(digital video player) 등 사용자가 휴대하여 이동하면서 사용할 수 있는 각종 기기를 의미할 수 있다. 또한, 이들 각종 기기들이 서로 통신으로 연결될 경우, 이들의 조합을 의미할 수 있다. 여기서, 사용자는 해당 단말을 사용하는 사람을 의미한다.Throughout the specification, a terminal includes software applications/programs stored in a computer-readable storage medium, and hardware such as a processor, memory, display, and communication module. The processor cooperates with the hardware to run the application. The display may display a user interface screen provided by an application. Depending on the terminal type, the display may receive a user input, for example, a touch input. The communication module may include device to device (D2D) communication between devices. In addition, the terminal may include a communication module capable of communicating with the server through a communication network. The terminal may be implemented in various forms, such as a tablet PC capable of communication, a wireless phone, a mobile phone, a smart phone, a smart watch, and smart glasses ( smart glass), e-book reader, PMP (portable multimedia player), portable game machine, navigation device, digital camera, DMB (digital multimedia broadcasting) player, digital audio recorder, digital It can refer to various devices that users can carry and use while moving, such as digital audio players, digital picture recorders, digital picture players, and digital video players. there is. Also, when these various devices are communicatively connected to each other, it may mean a combination thereof. Here, a user means a person who uses a corresponding terminal.

명세서 전체에서 결제장치는 통신이 가능한 태블릿(tablet) PC, 포스기(point of sales, POS), 무선전화기(wireless phone), 모바일 폰(mobile phone), 스마트 폰(smart phone), 스마트 워치(smart watch), 스마트 글래스(smart glass), e-book 리더기, PMP(portable multimedia player), 휴대용 게임기, 네비게이션(navigation) 장치, DMB(digital multimedia broadcasting) 재생기, 블루투스 장치, 단말 간 직접(device to device, D2D) 통신 장치 등 결제 수행이 가능한 각종 기기를 의미할 수 있다. 또한, 이들 각종 기기들이 서로 통신으로 연결될 경우, 이들의 조합을 의미할 수 있다.Throughout the specification, payment devices include a tablet PC capable of communication, a point of sales (POS), a wireless phone, a mobile phone, a smart phone, and a smart watch. watch), smart glass, e-book reader, PMP (portable multimedia player), portable game device, navigation device, DMB (digital multimedia broadcasting) player, Bluetooth device, device to device, D2D) may refer to various devices capable of performing payment, such as a communication device. Also, when these various devices are communicatively connected to each other, it may mean a combination thereof.

어플리케이션은 컴퓨터 판독 가능한 저장 매체에 저장되는 소프트웨어로서, 본 개시의 동작을 실행하는 명령어들(instructions) 및 데이터를 포함한다. 어플리케이션은 단말에 설치되고, 단말에서 실행된다. 또한 어플리케이션은 통신망을 통해 지정된 서버와 통신할 수 있거나 혹은 단말간 직접(device to device, D2D) 통신으로 다른 단말이나 장치와 통신할 수 있다. 이하에서 어플리케이션을 간단히 앱으로 지칭할 수 있다.An application is software stored on a computer-readable storage medium, and includes instructions and data for executing the operations of the present disclosure. The application is installed in the terminal and executed in the terminal. In addition, the application may communicate with a designated server through a communication network or may communicate with other terminals or devices through device-to-device (D2D) communication. Hereinafter, an application may simply be referred to as an app.

서버는 하나 이상의 프로세서, 프로세서에 의하여 수행되는 컴퓨터 프로그램을 로드하는 메모리, 컴퓨터 프로그램 및 각종 데이터를 저장하는 저장 장치, 통신 인터페이스를 포함할 수 있다.The server may include one or more processors, a memory for loading a computer program executed by the processor, a storage device for storing the computer program and various data, and a communication interface.

이하, 첨부한 도면들을 참조하여, 본 개시의 바람직한 실시예를 보다 상세하게 설명하고자 한다. 본 개시를 설명함에 있어 전체적인 이해를 용이하게 하기 위하여 도면상의 동일한 구성요소에 대해서는 동일한 참조부호를 사용하고 동일한 구성요소에 대해서 중복된 설명은 생략한다.Hereinafter, with reference to the accompanying drawings, preferred embodiments of the present disclosure will be described in more detail. In order to facilitate overall understanding in describing the present disclosure, the same reference numerals are used for the same components in the drawings, and redundant descriptions of the same components are omitted.

도 1은 본 발명의 일 실시예에 따른, 간편페이 결제 동작에 필요한 시스템 구성도이며, 동시에 일반적인 결제 관련 구성을 보여준다. 도 1을 참조하면, 단말(101)은 사용자(104)에 의하여 휴대가 가능한 장치 혹은 장치들의 조합일 수 있다. 결제장치(102)는 결제가능한 장치 혹은 이들의 조합일 수 있다. 또, 단말(101) 및 결제장치(102)는 사용자(104)에게 결제 금액을 알려주는 화면을 포함할 수 있고, 화면은 터치 입력이 가능한 화면일 수 있다. 보통 결제장치(102)는 유무선 통신을 통해서 결제시스템(103)에 연결되어 결제를 수행할 수 있다. 예를 들어, 신용카드를 사용하여 결제가 이루어질 경우, 결제시스템(103)은 인터넷에 연결된 해당 카드사의 서버를 포함할 수 있다. 여기서, 단말(101) 및 결제장치(102)는 단말간(device to device, D2D) 통신을 통해 패킷 혹은 비콘 혹은 시그널 혹은 펄스 등등의 무선 신호를 송수신할 수 있다. 또한, D2D 통신은 TDMA(time division multiple access) 기반의 통신 프로토콜 등을 지원할 수 있다.1 is a system configuration diagram necessary for a simple pay payment operation according to an embodiment of the present invention, and at the same time shows a general payment-related configuration. Referring to FIG. 1 , a terminal 101 may be a device that can be carried by a

도 1에서 단말(101)이 단말간 통신으로 카드 번호와 같은 사용자(104)의 결제 정보를 결제장치(102)에 전달하면, 결제장치(102)는 이를 이용하여 결제시스템(103)과 결제를 수행할 수 있다. 도 1은 매우 간략한 시스템 구성도이며, 결제장치(102)와 결제시스템(103)의 관계는 더 복잡할 수 있으나, 본 발명은 단말(101)과 결제장치(102) 간의 동작 방법에 관계되어 있기 때문에, 결제장치(102)와 결제시스템(103)은 간략하게 도 1에 표현되었다. 향후, 본 발명에서는 주로 단말(101)과 결제장치(102) 간의 절차에 초점을 맞춘다. 또한, 도 1에서 사용자(104)는 단말(101)을 사용하는 사람일 수 있다. 일반적으로 단말(101)의 소유자가 자신의 단말을 사용하며, 본 발명에서는 상기 단말의 적법한 소유자가 단말(101)을 사용한다고 가정한다.In FIG. 1, when the terminal 101 transmits payment information of the

현재 상용화된 D2D 통신들에는 블루투스(bluetooth), 비접촉 근거리 통신(near field communication, NFC), 초광대역(ultra-wideband, UWB), 와이파이 다이렉트(wifi-direct), 마그네틱 보안 전송(magnetic secure transmission, MST) 및 기타 여러 통신들이 있지만, 도 1에서 단말(101)과 결제장치(102)간의 통신에는 현재 주로 MST와 NFC 방식이 많이 사용되고 있다. 본 발명은 상기 상용화된 D2D 통신 수단들을 사용하여 구성될 수 있고, 또한 향후 상용화되는 D2D 통신 수단을 사용하여 구성될 수도 있다.Currently commercialized D2D communications include Bluetooth, near field communication (NFC), ultra-wideband (UWB), wifi-direct, and magnetic secure transmission (MST). ) and various other communications, but in FIG. 1 , MST and NFC methods are mainly used for communication between the terminal 101 and the

먼저, 본 발명의 이해를 돕기 위해서, 도 2와 도 3을 이용하여 현재 사용되고 있는 삼성페이와 애플페이를 서술한다.First, in order to help the understanding of the present invention, Samsung Pay and Apple Pay currently used will be described using FIGS. 2 and 3 .

도 2는 삼성페이의 동작 절차도이다. 본 발명은 사용자(104) 입장에서의 편의성을 증진시키는 것을 목적으로 하기 때문에, 절차도에서 사용자(104)가 직접 수행하는 부분은 점선으로 표시하고, 그 이외에는 실선으로 표시하여 사용자(104)의 경험을 알 수 있도록 구분한다.2 is a flowchart illustrating an operation of Samsung Pay. Since the present invention aims to enhance the convenience of the

도 2를 참조하면, 삼성페이는 사용자(104)가 단말(101)에 해당하는 스마트폰을 켜는 것으로부터 시작한다(S201). 이후 잠금을 해제하고(S202), 삼성페이 앱을 실행하고(S203), 사용자(104)인증을 수행하고(S204), 스마트폰을 결제장치(102)에 근접시킨다(S205). 그러면, 결제장치(102)가 스마트폰으로부터 결제 정보를 송수신하고 결제시스템(103)과 통신을 수행하여 결제를 수행한다(S206).Referring to FIG. 2 , Samsung Pay starts when the

스마트폰을 켜는 것(S201)은 일반적으로 전원 버튼을 누르거나 화면을 탭하는 동작에 의하여 수행된다. 일반적으로‘탭’은 화면을 살짝 두드리거나 터치하는 등의 동작을 의미한다. 잠금을 해제하는 것(S202)은 패턴 입력, 지문 인식, 안면 인식, 비밀번호 입력에 의하여 이루어질 수 있다. 이러한 입력 방법은 현재 스마트폰에서 널리 상용화된 방법들이다. 만약 사용자(104)가 스마트 워치를 사용한다면 잠금 해제는 자동으로 이루어질 수 있다. 삼성페이 앱을 실행하는 것(S203)은 사용자(104)가 직접 삼성페이 아이콘을 찾아서 탭을 함으로써 이루어진다. 사용자 인증(S204)은 잠금 해제(S202)와 비슷하게 비밀번호 입력 등으로 이루어질 수 있다. 사용자 인증(S204)이 완료되면, 사용자(104)의 스마트폰 화면이 바뀌면서 카드리더기에 휴대전화 뒷면을 대라는 안내가 나온다. 사용자(104)가 스마트폰을 결제장치(102)에 근접시키는 것(S205)은 스마트폰과 결제장치(102)가 보통 10cm 이내로 근접하는 것을 의미한다. 결제가 수행되는 것(S206)은 결제장치(102)가 결제시스템(103)과 결제를 수행하는 것을 의미한다. 이와 같이 삼성페이의 겨우, 다섯 단계를 사용자(104)가 수행해야 한다. 또한, 도 2에 표현되지 않았지만, 삼성페이의 경우 이동통신과의 데이터 통신이 활성화되어 있어야 한다. 그렇지 않다면, 사용자(104)는 이동통신과의 데이터 통신을 활성화하는 단계를 추가로 수행해야 한다.Turning on the smartphone (S201) is generally performed by pressing the power button or tapping the screen. In general, 'tap' means an action such as tapping or touching the screen. Unlocking (S202) may be performed by pattern input, fingerprint recognition, face recognition, or password input. These input methods are currently widely used in smart phones. If the

도 3은 애플페이의 동작 절차도이다. 절차도에서 사용자(104)가 직접 수행하는 부분은 점선으로 표시하고, 그 이외에는 실선으로 표시하여 사용자(104)의 경험을 알 수 있도록 구분한다.3 is an operation procedure diagram of Apple Pay. In the procedure diagram, the part that the

도 3을 참조하면, 애플페이는 사용자(104)가 단말(101)에 해당하는 스마트폰을 켜는 것으로부터 시작한다(S301). 이후 잠금을 해제하고(S302), 스마트폰을 결제장치(102)에 근접시킨다(S303). 그러면, 결제장치(102)가 스마트폰으로부터 결제 정보를 수신하고 결제를 수행한다(S304).Referring to FIG. 3 , Apple Pay starts when the

애플페이에서 스마트폰을 켜는 것(S301)은 일반적으로 전원 버튼을 두 번 누르는 것에 의하여 수행된다. 그러면, 이것은 보통의 스마트폰을 켜면서 동시에 애플페이를 실행하게 된다. 잠금을 해제하는 것(S302)은 패턴 입력, 지문 인식, 안면 인식, 비밀번호 입력에 의하여 이루어진다. 만약 사용자(104)가 스마트 워치를 사용한다면 잠금 해제는 자동으로 이루어질 수 있다. 삼성페이와 달리 애플페이는 잠금을 해제하는 것(S302) 만으로도 결제를 수행할 수 있다. 잠금 해제가 완료되면, 사용자(104)의 스마트폰 화면이 바뀌면서 카드리더기에 휴대전화 뒷면을 대라는 안내가 나온다. 사용자(104)가 스마트폰을 결제장치(102)에 근접시키는 것(S303)은 스마트폰과 결제장치(102)가 보톤 10cm 이내로 근접하는 것을 의미한다. 결제가 수행되는 것(S304)은 결제장치(102)가 결제시스템(103)과 결제를 수행하는 것을 의미한다. 이와 같이 애플페이는 삼성페이에 비해서 사용자(104)가 결제를 위해 수행하는 단계의 수가 3 단계이기 때문에 더 간편하다.Turning on the smartphone in Apple Pay (S301) is generally performed by pressing the power button twice. Then, it will launch Apple Pay at the same time as turning on a normal smartphone. Unlocking (S302) is performed by pattern input, fingerprint recognition, face recognition, and password input. If the

도 4는 본 발명의 일 실시예에 따른, 간편페이의 동작 흐름도이다. 흐름도에서 사용자(104)가 직접 수행하는 부분은 점선으로 표시하고, 그 이외에는 실선으로 표시하여 사용자(104)의 경험을 알 수 있도록 구분한다. 도 4에서 예외적으로 결제장치(102) 인식 단계(S401)는 사용자(104)가 직접 수행할 수도 있고 그렇지 않을 수도 있다.4 is an operation flow chart of Simple Pay according to an embodiment of the present invention. In the flow chart, the part that the

본 발명이 제안하는 간편페이는 사용자(104)가 스마트폰 같은 단말(101)을 꺼짐 화면 혹은 잠금 화면 상태에서 사용할 수 있어 삼성페이나 애플페이보다 더 간편한 사용자(104) 편의를 제공할 수 있다. 여기서, 단말(101)이 꺼짐 화면 상태라는 것은 사용자(104)가 단말(101)을 사용하지 않기 때문에 화면이 꺼져 있거나 혹은 절전을 위해서 시계와 같이 화면의 아주 일부분만 켜져 있는 상태를 의미할 수 있다. 예를 들어, 삼성 갤럭시 S22 스마트폰은 꺼짐 화면 상태에서도 시계와 날짜 및 문자 팝업 등을 제공하며, 그러한 설정은 ‘Always On Display’ 라는 이름으로 제공된다. 단말(101)이 잠금 화면 상태라는 것은 사용자(104)에 의하여 화면이 꺼짐 상태에서 켜짐 상태로 바뀌었지만, 사용자(104)가 사용자 인증을 수행해야 하는 상태를 의미한다. 예를 들어, 보통 스마트폰의 전원 버튼을 누르면 화면이 바로 켜지게 되는데, 이 잠금 화면 상태에서 사용자(104)가 지문 인식, 안면 인식, 패턴 입력, 비밀번호 입력 등의 사용자 인증 작업을 수행해야 스마트폰을 사용할 수 있고, 잠금 화면이 해제된다.The simple pay proposed by the present invention allows the

도 4를 참조하면, 단말(101)이 결제장치(102)를 인식하는 단계(S401)에서 단말(101)은 결제장치(102)의 존재를 인식할 수 있다. 결제 준비 정보를 무선으로 주고받는 단계(S402)에서 단말(101)은 결제장치(102)와 결제 가게 이름과 결제 금액 등의 결제와 관련된 정보를 교환할 수 있다. 단말(101)의 화면에 결제 정보를 표시하는 단계(S403)에서 단말(101)은 결제장치(102)로부터 받은 결제 관련 정보를 화면에 표시하여 사용자(104)에게 알릴 수 있다. 사용자 인증 단계(S404)에서는 사용자(104)가 단말(101)에 상기 단말(101)의 화면에 표시된 내용의 결제를 승인하기 위하여 사용자 인증을 수행할 수 있다. 결제 수행 단계(S405)에서는 결제장치(102)가 단말(101)로부터 카드 정보와 같은 결제 실행 정보를 송수신하고 결제시스템(103)과 통신을 수행하여 결제를 수행할 수 있다. 5가지 단계 중에서 사용자(104)가 관여하는 단계는 사용자 인증 단계(S404)이며, 인식 단계(S401)의 경우, 사용자(104)가 관여하는 방법도 있고 관여하지 않는 방법도 있다. 따라서, 도 4에서 제안되는 간편페이는 사용자(104)가 결제를 위해 수행하는 단계가 1 단계 혹은 2 단계이기 때문에 삼성페이나 애플페이보다 훨씬 더 편리하게 느껴질 수 있다.Referring to FIG. 4 , in step S401 in which the terminal 101 recognizes the

단말(101)이 결제장치(102)를 인식하는 단계(S401)에서, 단말(101)이 결제장치(102)의 존재를 인식하기 위하여, 블루투스, NFC, MST, UWB, wifi-direct, RFID(Radio-Frequency Identification) 및 기타 D2D 통신들을 이용할 수 있다. 예를 들어, 블루투스나 UWB를 사용하는 결제장치(102)는 자신의 인식 정보를 방송할 수 있으며, 단말(101)은 결제장치(102)가 방송하는 인식 정보를 수신하고 결제장치(102)를 인식할 수 있다. 상술된 방식은 다른 여러 D2D 통신들을 이용해서도 수행될 수 있다. 여기서, 방송되는 인식 정보는 장치의 종류, 장치 식별자(identification, ID), 장치 버전, 장치가 제공하는 서비스 중에서 하나 이상을 포함할 수 있다.In step S401 of the terminal 101 recognizing the

결제장치(102)가 방송하는 인식 정보는 방송에 사용되는 D2D 통신에 따라 수 미터에서 수 십 미터까지 수신될 수 있기 때문에 실제 결제를 수행하지 않는 단말들에게도 전달되는 문제가 발생할 수 있다. 따라서, 상술된 문제를 해결하기 위해서, 단말(101)이 결제장치(102)를 D2D 통신을 이용하여 인식할 때, 단말(101)이 결제장치(102)에 미리 정한 임계 거리 이내로 근접할 때만 결제장치(102)를 인식할 수 있다. 2021년부터 갤럭시 S21 울트라 같은 스마트폰 모델은 UWB 가 탑재되어 판매되고 있는데, 결제장치(102)에 UWB 가 탑재된다면, 결제장치(102)와 스마트폰의 거리는 UWB 를 사용하여 매우 정확하게 측정될 수 있다. 현재 UWB 의 거리 오차는 cm(센치미터) 단위의 매우 정교한 수준으로 알려져 있다. 상술한 문제를 해결하기 위하여, 단말(101)이 결제장치(102)를 D2D 통신을 이용하여 인식할 때, 결제장치(102)가 전송하는 무선 신호의 수신 파워가 미리 정한 임계 파워보다 높을 때만 결제장치(102)를 인식할 수 있다. 이것은 UWB 외의 다른 통신 방식에서 더 유용한 방식이며, 수신 파워가 높다는 것은 결제장치(102)와 단말(101)이 가까이 있다는 것을 의미할 수 있다. 상술한 문제를 해결하는 또다른 방법은 단말(101)이 내장한 D2D 통신 장치가 결제장치(102)가 전송하는 무선 신호에 의하여 활성화될 때 결제장치(102)를 인식하는 것이다. 이것은 NFC 에 적합한 방식으로, 결제장치(102)의 NFC 리더기는 자기장을 발생시키고, 단말(101)의 NFC 장치는 결제장치(102)에 가까이 갔을 때 NFC 리더기의 자기장 신호에 의하여 활성화되어 NFC 리더기를 인식할 수 있다.Since recognition information broadcasted by the

상기 방식들과는 달리, 단말(101)이 결제장치(102)를 D2D 통신을 이용하여 인식하는 것은, 결제장치(102)가 단말(101)을 인식하고 단말(101)에게 결제 대상임을 통보함으로써 수행될 수 있다. 이를 위해서 단말(101)이 자신의 인식 정보를 D2D 통신으로 방송할 수 있다. 결제장치(102)는 단말(101)이 방송하는 인식 정보를 수신하여, 단말(101)을 인식할 수 있다. 이때, 인식되는 단말(101)이 여러 대일 경우, 거리가 가장 가깝거나 혹은 인식 신호의 수신 파워가 가장 큰 단말(101)을 선택할 수 있다. 이러한 선택 이후에, 결제장치(102)는 선택된 단말(101)에게 결제 대상임을 D2D 통신을 이용하여 통보할 수 있다. 단말(101)은 상술된 통보를 받음으로써 결제장치(102)를 인식할 수 있다. 예를 들어, 블루투스의 일종인 블루투스 저 에너지 (bluetooth low energy, BLE) 통신의 경우, 자신의 정보를 비콘 등으로 방송할 수 있고, 따라서 단말(101)과 결제장치(102)는 각각 자신의 인식 정보를 비콘으로 방송할 수 있다. 결제장치(102)는 단말(101)들이 BLE 로 방송하는 인식 정보를 수신하여 단말들을 인식하고, 가장 수신 파워가 큰 단말(101)에게 결제 대상임을 BLE 로 통보할 수 있다. 그러면, 결제 대상임을 통보받은 단말(101)은 상기 통보에 의하여 해당 결제장치(102)를 인식할 수 있다.Unlike the above methods, when the terminal 101 recognizes the

결제 준비 정보를 무선으로 주고받는 단계(S402)에서 단말(101)은 결제장치(102)와 결제를 준비하기 위한 정보를 주고받을 수 있다. 대표적으로, 결제장치(102)와 단말(101)이 주고받는 정보는 가게 이름, 결제할 금액, 결제할 물품의 목록, 할부 가능 정보, 사용 가능한 결제 수단 정보, 적립포인트 중의 결제가능한 금액, 사용가능한 할인 쿠폰, 사용자(104)의 나이, 가게 회원번호, 멤버쉽 회원 번호 등을 포함할 수 있다. 여기서, 사용자(104)의 나이는 담배 등의 물품을 살 때, 성인 인증 목적으로 요구될 수 있다. 결제와 관련되어 필요한 정보는 가게마다 혹은 물품마다 상당히 상이할 수 있다.In the step of wirelessly exchanging payment preparation information ( S402 ), the terminal 101 may exchange information for preparing payment with the

단말(101)의 화면에 결제 정보를 표시하는 단계(S403)에서 단말(101)은 결제장치(102)로부터 주고받은 결제 관련 정보와 단말(101)에 내장된 결제 수행에 필요한 정보 등을 화면에 표시하여 사용자(104)에게 알릴 수 있고, 이러한 알림은 단말(101)이 꺼짐 화면 상태이거나 잠금 상태에서도 동작할 수 있다. 예를 들어, 상술된 알림은 팝업창으로 제공될 수 있는데, 단말(101)이 꺼짐 화면 상태이거나 잠금 화면 상태에서도 해당 내용이 단말(101)의 화면에서 팝업창으로 제공될 수 있다. 여기서, ‘팝업창’이란 현재 화면 위에 추가적으로 어떠한 내용을 표시하기 위해 갑자기 생성되는 새 창을 의미할 수 있다. 예를 들면, 일반적인 스마트폰에서 문자 메지시가 오면, 현재 화면에 팝업창으로 해당 문자의 일부나 전부가 표시된다. 단말(101)의 화면에 표시되는 정보는 가게 이름, 결제할 금액, 할부 정보, 적립포인트 중의 결제가능한 금액, 사용 가능한 할인 쿠폰, 결제할 카드 번호, 카드 유효기간, 카드사 중의 하나 이상을 포함할 수 있다. 예를 들어, ‘싱싱마트 25,000 원 씨티카드로 결제하시겠습니까?’라는 팝업 문구가 뜰 수 있다.In the step of displaying payment information on the screen of the terminal 101 (S403), the terminal 101 transmits and receives payment related information from the

팝업창이 뜰 때, 단말(101)은 여러 카드를 내장할 수 있기 때문에, 팝업에는 다른 카드 선택을 위한 버튼이 표시될 수 있다. 그리고, 사용자(104)는 상기 버튼을 탭하여 다른 카드를 선택할 수 있다. 또, 사용자(104)는 할인 쿠폰이나 멤버쉽 카드도 마찬가지로 선택할 수 있다. 사용자(104)에 의한 결제 수단 선택은 이미 상용화된 일반적인 과정이다. 반면, 자동으로 할인 쿠폰이나 멤버쉽 카드를 선택하여 사용자(104)에게 표시해 주는 경우, 단말(101)은 S402 단계에서 할인 혹은 포인트 혹음 멤버쉽 관련 정보를 결제장치(102)로부터 수신하고, 단말(101)에 내장된 쿠폰이나 멤버쉽 카드가 있는 지 확인할 수 있다. 사용 가능한 쿠폰이나 할인되는 멤버쉽 카드가 있다면, 사용자(104)는 이를 선택할 수 있다. 혹은 편리한 결제를 위하여 사용자(104)는 사용가능한 쿠폰이나 기프티콘 혹은 할인되는 멤버쉽 카드의 자동 사용을 단말(101)에 설정할 수 있다. 이 경우, 화면 팝업에는 자동으로 사용되는 할인 쿠폰이나 멤버쉽 카드 정보가 함께 표시될 수 있다. 예를 들어, ‘싱싱마트 22,500 원 씨티카드로 결제하시겠습니까? 씨티 멤버쉽 할인 10% (2500원) 적용’ 라는 팝업 문구가 뜰 수 있다.When a pop-up window appears, since the terminal 101 can store several cards, a button for selecting another card may be displayed on the pop-up window. Then, the

결제 정보를 표시하는 단계(S403)에서, 사용자(104)는 결제 정보가 단말의 화면에 표시된 것을 쉽게 인지하지 못할 수 있다. 상술된 문제를 해결하기 위해서, 단말(101) 혹은 결제장치(102)가 알림음을 송출하거나 혹은 단말(101)이 알림 진동을 수행할 수 있다. 그러면, 사용자(104)는 상술된 알림을 인지하여 단말(101)의 화면을 바라보고, 사용자 인증(S404)을 수행할 수 있다.In the step of displaying the payment information (S403), the

사용자 인증 단계(S404)에서는 사용자(104)가 단말(101)에 사용자 인증을 위한 정보를 입력하는 것은, S403 단계에서 상기 팝업창과 함께 비밀번호 입력 혹은 패턴 입력이 함께 표시되면, 사용자(104)가 비밀번호나 패턴을 입력함으로써 수행될 수 있다. 하지만, 삼성이나 애플의 스마트폰들은 지문 인식이나 안면 인식 기능을 제공하기 때문에 이들에 의해서도 사용자 인증이 수행될 수 있다.In the user authentication step (S404), the

여기서, 사용자(104)가 비밀번호나 패턴을 입력할 때, 사용자(104)는 주변 다른 사람들에 의해서 본인의 비밀번호나 패턴이 알려질 수 있는 잠재적 위험에 노출될 수 있다. 하지만, 상기 설명된 알림음이나 알림 진동이 울린 이후에 사용자(104)는 결제장치(102)에 근접한 단말(101)을 다른 위치로 가져갈 수 있고, 이렇게 함으로써 상기 잠재적 위험 노출 위험을 상당히 감소시킬 수 있다. 일반적으로 단말(101)과 결제장치(102)가 근접했을 때, 둘 간의 보안이 설정될 수 있으므로, 사용자(104)가 단말(101)을 다른 위치로 가져가도 단말(101)과 결제장치(102)는 보안된 상태에서 통신을 수행할 수 있다. 본 발명은 구체적 보안 설정에 대해서는 상세한 기술을 하지 않는다.Here, when the

여러 사용자 인증 방법 중에서도, ‘지문 인식’은 특히 매우 편리한 인증 방법을 제공할 수 있다. 예를 들면, 사용자(104)가 지문 인식 상태에서 단말(101)을 결제장치(102)에 가까이 가져가는 것만으로 모든 결제 절차가 종료될 수 있다. 이것은 사용자(104)가 이미 결제장치(102)의 화면을 통해서 결제 금액과 내용을 알고 있고 동시에 자주 이용하는 결제 수단을 이미 단말(101)에 세팅해 놓았을 때 수행될 수 있다. 혹은 단말(101)의 결제 프로그램이 자동으로 결제 수단을 선택하는 경우에 수행될 수 있다. 즉, 사용자(104)의 지문이 지문 인식기에 접촉되고 있는 상태에서 스마트폰 같은 단말(101)이 결제장치(102)에 가까이 다가가면, 단말(101)과 결제장치(102) 간의 거리 혹은 인식 신호의 수신 파워 등을 이용하여 단말(101)이 결제장치(102)를 인식할 수 있고(S401), 결제 준비 정보를 무선으로 결제장치(102)와 주고받을 수 있고(S402), 결제 정보를 표시하는 단계(S403)는 생략되며, 사용자 인증 단계(S404)는 지문 인식기에 접촉되어 있는 지문에 의하여 수행된 후, 결제장치(102)가 단말(101)로부터 결제 실행 정보를 수신받아 결제시스템(103)과 통신하여 결제를 수행할 수 있다(S405). 이때, 단말(101)은 미리 세팅된 결제 수단과 관련된 결제 실행 정보를 결제장치(102)와 교환한다. 즉, 미리 세팅된 카드나 오픈 뱅킹 및 그 외 결제 수단과 관련된 정보를 교환할 수 있다. 특히, 상술된 사전 결제 수단 설정이 하나가 아닌 여러 개가 존재하는 경우, 지문 인식이 특히 편리하게 쓰일 수 있다. 즉, 사용자(104)는 보통 검지나 중지를 단말(101) 지문 인식기에 댈 수 있으며, 이것은 오른손과 왼손이 모두 가능하다. 따라서, 사용자(104)가 편리하게 인식시킬 수 있는 지문은 대략 4개가 존재하며, 각 지문마다 4개의 다른 결제 수단을 미리 세팅해 놓을 수 있다. 단말(101)은 인증에 사용된 지문이 어떤 것인지 판단해서 상기 인증에 사용된 지문과 미리 매핑된 결제 수단을 결제에 사용할 수 있다. 예를 들면, 오른 손 검지를 사용한 결제에서는 ‘씨티 카드’를 사용하고, 오른 손 중지를 사용한 결제에서는 ‘삼성 카드’를 사용하는 것으로 미리 설정될 수 있다. 한편, 꺼짐 화면이나 잠금 화면 상태에서 지문인식은 화면 잠금 해제와 화면 켜짐 및 결제 인증에 함께 쓰일 수 있다. 즉, 사용자(104)는 지문이 인식될 때 잠금 해제와 화면 켜짐이 실행되도록 단말(101)을 설정할 수 있고, 그렇게 설정한 경우, 간편한 결제를 수행하기 위하여 사용자(104)가 꺼짐 화면이나 잠금 화면 상태에서 단말의 지문 인식기에 손가락을 대고 결제를 수행하는 동작은 화면 켜짐과 잠금 해제를 유발할 수 있다.Among several user authentication methods, 'fingerprint recognition' can provide a particularly convenient authentication method. For example, all payment procedures may be terminated when the

상기와 같이 지문인식이 사용될 때, 사용자(104)가 단말(101)에 미리 입력한 결제 세팅에 따라, 결제 정보를 표시하는 단계(S403)가 수행될 수도 있다. 예를 들면, 단말(101)에 표시되는 팝업창의 내용은 ‘싱싱마트 25,000 원 씨티카드로 결제를 요청하는 중입니다’로 표시될 수 있다. 따라서, 사용자(104)는 현재 결재가 요청 중임을 쉽게 알 수 있다.When fingerprint recognition is used as described above, the step of displaying payment information (S403) may be performed according to the payment setting input by the

결제 수행 단계(S405)에서 결제장치(102)와 단말(101)은 카드 정보와 같은 결제 실행 정보를 송수신하고, 결제장치(102)는 상기 송수신한 결제 실행 정보를 이용하여 결제시스템(103)과 결제를 수행할 수 있다. 이 단계에서 단말(101)은 현재 일반적으로 이루어지고 있는 MST 통신이나 NFC 통신을 사용할 수 있고, 또 향후 UWB 혹은 블루투스와 같은 다른 D2D 통신을 사용할 수 있다. UWB 혹은 블루투스 등의 D2D 통신은 통신 거리가 길기 때문에, 상기 단계에서 사용자(104)가 단말(101)을 다시 결제장치에 가까이 가져가지 않을 수 있다. 하지만, MST 나 NFC 통신의 경우 통신 거리가 짧기 때문에, 사용자(104)가 단말(101)을 다시 결제장치(102)에 가까이 가져가야 할 수 있다. 결제장치(102)가 결제시스템(103)과 통신을 수행하여 결제를 수행하는 것은 현재의 과정과 동일하게 구현될 수 있다.In the payment execution step (S405), the

도 5은 본 발명의 일 실시예에 따른, 간편페이의 확장 동작 흐름도이다. 도 5와 도 4를 참조하면, S501~S505 는 S401~S405와 같다. 도 5를 참조하면, 결제 수행 단계(S505)에서 결제가 완료되면, 결제 승인 완료 표시 단계(S506)에서, 단말(101)은 결제장치(102)로부터 결제에 대한 승인 완료 정보를 D2D 통신으로 수신하여 이를 단말(101)의 화면에 표시할 수 있다. 예를 들면, ‘싱싱마트 25,000 원 씨티카드로 결제 완료되었습니다. 250원이 적립되었습니다.’ 등으로 표시될 수 있다. 물론, 카드사에서는 결제 완료 정보를 사용자(104)에게 이동통신을 이용한 문자로 제공하기도 한다. 하지만, 상술된 서비스는 유료인 경우가 많기 때문에, 결제장치(102)가 결제에 대한 승인 완료 정보를 단말(101)에 전송하면, 유료 서비스를 대체할 수 있다.5 is a flowchart of an expansion operation of a simple pay according to an embodiment of the present invention. Referring to FIGS. 5 and 4 , S501 to S505 are the same as S401 to S405. Referring to FIG. 5 , when the payment is completed in the payment execution step (S505), the terminal 101 receives payment approval completion information from the

영수증 수신 단계(S507)에서 단말(101)은 결제장치(102)로부터 결제에 대한 영수증을 D2D 통신으로 수신하여 이를 단말(101)의 화면에 표시할 수 있다. 상술된 전자 영수증 수신은 사용자(104)가 구매 목록을 편리하게 알 수 있게 도와주며, 특히 환불을 원할 경우 유용하게 사용될 수 있다. 보통 영수증은 종이로 출력되고, 단말(101)에 이동통신을 통해서 문자로 오는 경우는 거의 없다. 따라서, S507 단계는 종이 사용을 줄일 수 있다.In the receipt receiving step (S507), the terminal 101 may receive a receipt for payment from the

영수증 송신 단계(S508)에서 단말(101)은 결제장치(102)에게 S507 단계에서 수신한 결제 영수증을 송신하여 이를 결제장치(102)의 화면에 표시할 수 있다. 상술된 방법은 사용자(104)가 환불을 원할 경우 유용하게 사용될 수 있다. 일반적으로 영수증 송신 단계(S508)는 생략될 수 있으며, 이 경우 영수증 수신 단계(S507) 혹은 결제 승인 완료 표시 단계(S506)에서 흐름도가 종료될 수 있다.In the receipt transmission step (S508), the terminal 101 may transmit the payment receipt received in step S507 to the

도 6은 본 발명의 일 실시예에 따른, 간편페이에 사용되는 단말(101)의 블록도이다. 도 6에서, 단말에 101과 다른 600의 부호가 부여되었으나, 101과 600은 모두 같은 단말을 의미한다.6 is a block diagram of a terminal 101 used for simple pay according to an embodiment of the present invention. In FIG. 6, a code of 600 different from 101 is given to the terminal, but both 101 and 600 mean the same terminal.

도 6을 참조하면, 단말(600)은 적어도 하나의 프로세서(610), 메모리(620), 네트워크와 연결되어 통신을 수행하는 송수신 장치(630) 및 D2D 통신을 수행하는 D2D 장치(640)를 포함할 수 있다. 또한, 단말(600)은 입력 인터페이스 장치(650), 출력 인터페이스 장치(660), 저장 장치(670) 등을 더 포함할 수 있다. 단말(600)에 포함된 각각의 구성 요소들은 버스(bus)(680)에 의해 연결되어 서로 통신을 수행할 수 있다. 다만, 단말(600)에 포함된 각각의 구성요소들은 공통 버스(680)가 아니라, 프로세서(610)를 중심으로 개별 인터페이스 또는 개별 버스를 통하여 연결될 수도 있다. 예를 들어, 프로세서(610)는 메모리(620), 송수신 장치(630), D2D 장치(640), 입력 인터페이스 장치(650), 출력 인터페이스 장치(660) 및 저장 장치(670) 중에서 적어도 하나와 전용 인터페이스를 통하여 연결될 수도 있다.Referring to FIG. 6 , a terminal 600 includes at least one

프로세서(610)는 메모리(620) 및 저장 장치(670) 중에서 적어도 하나에 저장된 프로그램 명령(program command)을 실행할 수 있다. 프로세서(610)는 중앙 처리 장치(central processing unit, CPU), 그래픽 처리 장치(graphics processing unit, GPU), 또는 본 발명의 실시예들에 따른 방법들이 수행되는 전용의 프로세서를 의미할 수 있다. 메모리(620) 및 저장 장치(670) 각각은 휘발성 저장 매체 및 비휘발성 저장 매체 중에서 적어도 하나로 구성될 수 있다. 예를 들어, 메모리(620)는 읽기 전용 메모리(read only memory, ROM) 및 랜덤 액세스 메모리(random access memory, RAM) 중에서 적어도 하나로 구성될 수 있다.The

본 개시의 실시 예에 따른 방법의 동작은 컴퓨터로 읽을 수 있는 기록매체에 컴퓨터가 읽을 수 있는 프로그램 또는 코드로서 구현하는 것이 가능하다. 컴퓨터가 읽을 수 있는 기록매체는 컴퓨터 시스템에 의해 읽혀질 수 있는 정보가 저장되는 모든 종류의 기록장치를 포함한다. 또한 컴퓨터가 읽을 수 있는 기록매체는 네트워크로 연결된 컴퓨터 시스템에 분산되어 분산 방식으로 컴퓨터로 읽을 수 있는 프로그램 또는 코드가 저장되고 실행될 수 있다.The operation of the method according to an embodiment of the present disclosure can be implemented as a computer readable program or code on a computer readable recording medium. A computer-readable recording medium includes all types of recording devices in which information that can be read by a computer system is stored. In addition, computer-readable recording media may be distributed to computer systems connected through a network to store and execute computer-readable programs or codes in a distributed manner.

또한, 컴퓨터가 읽을 수 있는 기록매체는 롬(rom), 램(ram), 플래시 메모리(flash memory) 등과 같이 프로그램 명령을 저장하고 수행하도록 특별히 구성된 하드웨어 장치를 포함할 수 있다. 프로그램 명령은 컴파일러(compiler)에 의해 만들어지는 것과 같은 기계어 코드뿐만 아니라 인터프리터(interpreter) 등을 사용해서 컴퓨터에 의해 실행될 수 있는 고급 언어 코드를 포함할 수 있다.In addition, the computer-readable recording medium may include hardware devices specially configured to store and execute program instructions, such as ROM, RAM, and flash memory. The program command may include high-level language codes that can be executed by a computer using an interpreter or the like as well as machine code generated by a compiler.

본 개시의 일부 측면들은 장치의 문맥에서 설명되었으나, 그것은 상응하는 방법에 따른 설명 또한 나타낼 수 있고, 여기서 블록 또는 장치는 방법 단계 또는 방법 단계의 특징에 상응한다. 유사하게, 방법의 문맥에서 설명된 측면들은 또한 상응하는 블록 또는 아이템 또는 상응하는 장치의 특징으로 나타낼 수 있다. 방법 단계들의 몇몇 또는 전부는 예를 들어, 마이크로프로세서, 프로그램 가능한 컴퓨터 또는 전자 회로와 같은 하드웨어 장치에 의해(또는 이용하여) 수행될 수 있다. 몇몇의 실시 예에서, 가장 중요한 방법 단계들의 적어도 하나 이상은 이와 같은 장치에 의해 수행될 수 있다.Although some aspects of the present disclosure have been described in the context of an apparatus, it may also represent a description according to a corresponding method, where a block or apparatus corresponds to a method step or feature of a method step. Similarly, aspects described in the context of a method may also be represented by a corresponding block or item or a corresponding feature of a device. Some or all of the method steps may be performed by (or using) a hardware device such as, for example, a microprocessor, programmable computer, or electronic circuitry. In some embodiments, at least one or more of the most important method steps may be performed by such a device.

실시 예들에서, 프로그램 가능한 로직 장치(예를 들어, 필드 프로그래머블 게이트 어레이)가 여기서 설명된 방법들의 기능의 일부 또는 전부를 수행하기 위해 사용될 수 있다. 실시 예들에서, 필드 프로그래머블 게이트 어레이(field-programmable gate array)는 여기서 설명된 방법들 중 하나를 수행하기 위한 마이크로프로세서(microprocessor)와 함께 작동할 수 있다.In embodiments, a programmable logic device (eg, a field programmable gate array) may be used to perform some or all of the functions of the methods described herein. In embodiments, a field-programmable gate array may operate in conjunction with a microprocessor to perform one of the methods described herein.

이상 본 개시의 바람직한 실시 예를 참조하여 설명하였지만, 해당 기술 분야의 숙련된 당업자는 하기의 특허 청구의 범위에 기재된 본 개시의 사상 및 영역으로부터 벗어나지 않는 범위 내에서 본 개시를 다양하게 수정 및 변경시킬 수 있음을 이해할 수 있을 것이다.Although it has been described with reference to the preferred embodiments of the present disclosure, those skilled in the art can variously modify and change the present disclosure within the scope not departing from the spirit and scope of the present disclosure described in the claims below. You will understand that you can.

Claims (18)

Translated fromKorean꺼짐 화면 혹은 잠금 화면 상태에서 단말간 통신을 이용하여 결제장치를 인식하는 단계;

상기 결제장치와 결제 준비 정보를 무선으로 주고받는 단계;

제1 단말의 화면에 상기 결제 정보가 표시되는 단계;

사용자로부터 사용자 인증 정보를 입력받는 단계; 및

상기 결제장치에게 상기 결제의 실행 정보를 전송하는 단계를 포함하는,

제1 단말의 동작 방법

As a method of operating a first terminal in which a simple pay application is installed,

Recognizing a payment device using device-to-device communication in an off-screen or lock-screen state;

wirelessly exchanging payment preparation information with the payment device;

displaying the payment information on a screen of a first terminal;

Receiving user authentication information from a user; and

Transmitting execution information of the payment to the payment device,

Operation method of the first terminal

제1 단말이 상기 결제장치를 인식하기 위하여 사용하는 단말간 통신은 블루투스(bluetooth), 비접촉 근거리 통신(near field communication, NFC), 마그네틱 보안 전송(magnetic secure transmission, MST), 초광대역(ultra-wideband, UWB) 통신, 와이파이 다이렉트(wifi-direct) 중의 하나인,

제1 단말의 동작 방법

According to claim 1,

Terminal-to-device communication used by the first terminal to recognize the payment device includes Bluetooth, near field communication (NFC), magnetic secure transmission (MST), and ultra-wideband. , UWB) communication, which is one of wifi-direct,

Operation method of the first terminal

상기 결제장치를 단말간 통신을 이용하여 인식하는 방법은,

제1 단말이 상기 결제장치가 단말간 통신을 이용하여 방송하는 결제장치 인식 정보를 수신하는 것인,

제1 단말의 동작 방법

According to claim 1,

The method for recognizing the payment device using terminal-to-device communication,

wherein the first terminal receives payment device identification information broadcast by the payment device using terminal-to-device communication;

Operation method of the first terminal

제1 단말이 상기 결제장치를 단말간 통신을 이용하여 인식하기 위한 조건은,

제1 단말이 상기 결제장치에 미리 정한 임계 거리 이내로 근접하거나 혹은 제1 단말에서 상기 결제장치가 전송하는 무선 신호의 수신 파워가 미리 정한 임계 파워보다 높거나 혹은 제1 단말의 단말간 통신 장치가 상기 결제장치가 전송하는 신호에 의하여 활성화되는 것인,

제1 단말의 동작 방법

According to claim 1,

The condition for the first terminal to recognize the payment device using terminal-to-device communication is,

The first terminal approaches the payment device within a predetermined threshold distance, or the first terminal receives power of a radio signal transmitted by the payment device is higher than a predetermined threshold power, or the terminal-to-device communication device of the first terminal which is activated by a signal transmitted by the payment device,

Operation method of the first terminal

제1 단말이 상기 결제장치를 단말간 통신을 이용하여 인식하는 방법은,

상기 결제장치로부터 결제 대상임을 통보받는 것인,

제1 단말의 동작 방법

According to claim 1,

The method in which the first terminal recognizes the payment device using terminal-to-terminal communication,

To be notified of the payment target from the payment device,

Operation method of the first terminal

제1 단말이 상기 결제장치로부터 결제 대상임을 통보받는 방법은,

상기 결제장치가 상기 결제장치로부터 가장 거리가 가까운 단말로 제1 단말을 선택하여 제1 단말에게 결제 대상임을 통지하는 단말간 통신 신호를 수신하거나, 혹은 상기 결제장치가 단말간 통신 신호의 수신 파워가 가장 큰 단말로 제1 단말을 선택하여 제1 단말에게 결제 대상임을 통지하는 단말간 통신 신호를 수신하는 것인,

제1 단말의 동작 방법

According to claim 5,

The method for the first terminal to be notified of the payment target from the payment device,

The payment device selects the first terminal as the terminal closest to the payment device and receives a terminal-to-terminal communication signal notifying the first terminal that it is a payment target, or the payment device has low reception power of the terminal-to-device communication signal Selecting the first terminal as the largest terminal and receiving a terminal-to-terminal communication signal notifying the first terminal that it is a payment target,

Operation method of the first terminal

상기 결제장치와 무선으로 주고받는 결제 준비 정보는,

가게 이름, 결제할 금액, 할부 정보, 적립포인트 중의 결제 가능한 금액, 사용 가능한 할인 쿠폰, 사용자 개인 정보 중의 하나 이상을 포함하는,

제1 단말의 동작 방법

According to claim 1,

The payment preparation information wirelessly exchanged with the payment device,

Including one or more of the shop name, amount to be paid, installment information, payment amount among points earned, available discount coupons, and user personal information,

Operation method of the first terminal

단말의 화면에 표시되는 상기 결제 정보는,

가게 이름, 결제할 금액, 결제할 카드 이름, 할부 정보, 적립포인트 중의 결제 가능한 금액, 사용 가능한 할인 쿠폰 중의 하나 이상을 포함하는,

제1 단말의 동작 방법

According to claim 1,

The payment information displayed on the screen of the terminal,

Including one or more of the store name, amount to be paid, card name to be paid, installment information, amount available for payment among accumulation points, and available discount coupons,

Operation method of the first terminal

제1 단말의 화면에 상기 결제 정보가 표시되는 방법은,

꺼짐 화면 혹은 잠금 화면 상태에서 팝업으로 표시되는 것인,

제1 단말의 동작 방법

According to claim 1,

The method of displaying the payment information on the screen of the first terminal,

which is displayed as a pop-up in the off screen or lock screen state,

Operation method of the first terminal

제1 단말이 사용자로부터 사용자 인증 정보를 입력받는 방법은,

지문 인식, 안면 인식, 패턴 인식, 비밀번호 입력 중의 하나 이상을 포함하는,

제1 단말의 동작 방법

According to claim 1,

A method in which the first terminal receives user authentication information from the user,

Including one or more of fingerprint recognition, face recognition, pattern recognition, and password input,

Operation method of the first terminal

제1 단말이 상기 결제장치를 인식하고 상기 결제장치와 결제 준비 정보를 무선으로 주고받을 때 사용자 인증이 제1 단말에서 수행되는 경우,

제1 단말은 사용자로부터 사용자 인증 정보를 입력받는 단계를 생략하는,

제1 단말의 동작 방법

According to claim 1,

When user authentication is performed in the first terminal when the first terminal recognizes the payment device and wirelessly exchanges payment preparation information with the payment device,

The first terminal omits the step of receiving user authentication information from the user,

Operation method of the first terminal

제1 단말이 상기 결제장치를 인식하고 상기 결제장치와 결제 준비 정보를 무선으로 주고받을 때 사용자 인증이 제1 단말에서 수행되는 경우,

제1 단말은 제1 단말의 화면에 상기 결제 정보가 표시되는 단계와 사용자로부터 사용자 인증 정보를 입력받는 단계를 동시에 생략하는,

제1 단말의 동작 방법

According to claim 1,

When user authentication is performed in the first terminal when the first terminal recognizes the payment device and wirelessly exchanges payment preparation information with the payment device,

The first terminal simultaneously omits the step of displaying the payment information on the screen of the first terminal and the step of receiving user authentication information from the user.

Operation method of the first terminal

제1 단말이 상기 결제장치를 인식하고 상기 결제장치와 결제 준비 정보를 무선으로 주고받을 때 사용자 인증이 제1 단말에서 수행되는 경우,

그 인증 수단이 지문이면, 제1 단말은 상기 인증에 사용된 지문과 미리 매핑(mapping)된 결제 수단을 상기 결제에 사용하는,

제1 단말의 동작 방법

According to claim 1,

When user authentication is performed in the first terminal when the first terminal recognizes the payment device and wirelessly exchanges payment preparation information with the payment device,

If the authentication means is a fingerprint, the first terminal uses a payment means pre-mapped with the fingerprint used for the authentication for the payment.

Operation method of the first terminal

꺼짐 화면 혹은 잠금 화면 상태에서 단말간 통신을 이용하여 결제장치를 인식하는 단계 이후에,

인식 알림음을 송출하거나 알림 진동을 수행하는 단계를 더 포함하는,

제1 단말의 동작 방법

According to claim 1,

After the step of recognizing the payment device using device-to-device communication in the off screen or lock screen state,

Further comprising the step of sending a recognition notification sound or performing a notification vibration,

Operation method of the first terminal

상기 결제장치에게 상기 결제의 실행 정보를 전송하는 단계 이후에,

상기 결제장치로부터 상기 결제에 대한 승인 완료 정보를 수신하여, 상기 수신한 정보를 제1 단말의 화면에 표시하는 단계를 더 포함하는,

제1 단말의 동작 방법

According to claim 1,

After the step of transmitting the payment execution information to the payment device,

Receiving approval completion information for the payment from the payment device, and displaying the received information on a screen of a first terminal,

Operation method of the first terminal

상기 결제장치에게 상기 결제의 실행 정보를 전송하는 단계 이후에,

상기 결제장치로부터 상기 결제에 대한 영수증을 수신하여, 상기 수신한 영수증을 제1 단말의 화면에 표시하는 단계를 더 포함하는,

제1 단말의 동작 방법

According to claim 1,

After the step of transmitting the payment execution information to the payment device,

Receiving a receipt for the payment from the payment device and displaying the received receipt on a screen of a first terminal,

Operation method of the first terminal

상기 결제장치로부터 상기 결제에 대한 영수증을 수신하는 단계 이후에,

상기 수신한 결제 영수증을 상기 결제장치의 화면에 표시하기 위하여 상기 결제장치에게 송신하는 단계를 더 포함하는,

제1 단말의 동작 방법

According to claim 16,

After receiving a receipt for the payment from the payment device,

Further comprising transmitting the received payment receipt to the payment device to display on the screen of the payment device.

Operation method of the first terminal

꺼짐 화면 혹은 잠금 화면 상태에서 단말간 통신을 이용하여 결제장치를 인식하는 기능;

상기 결제장치와 결제 준비 정보를 무선으로 주고받는 기능;

제1 단말의 화면에 상기 결제 정보가 표시되는 기능;

사용자로부터 사용자 인증 정보를 입력받는 기능; 및

상기 결제장치에게 상기 결제의 실행 정보를 전송하는 기능을 포함하는,

어플리케이션

As an application stored in a recording medium that allows a terminal to perform the following functions, the functions include:

A function of recognizing a payment device using device-to-device communication in an off-screen or lock-screen state;

a function of wirelessly exchanging payment preparation information with the payment device;

a function of displaying the payment information on a screen of a first terminal;

A function of receiving user authentication information from a user; and

Including a function of transmitting execution information of the payment to the payment device,

application

Priority Applications (3)

| Application Number | Priority Date | Filing Date | Title |

|---|---|---|---|

| KR1020230068756AKR20230106533A (en) | 2023-05-27 | 2023-05-27 | Method and application for easy payment in mart |

| KR1020230104605AKR20240170748A (en) | 2023-05-27 | 2023-08-10 | Method and application for easy payment |

| PCT/KR2024/004777WO2024248316A1 (en) | 2023-05-27 | 2024-04-09 | Simple payment method and application |

Applications Claiming Priority (1)

| Application Number | Priority Date | Filing Date | Title |

|---|---|---|---|

| KR1020230068756AKR20230106533A (en) | 2023-05-27 | 2023-05-27 | Method and application for easy payment in mart |

Publications (1)

| Publication Number | Publication Date |

|---|---|

| KR20230106533Atrue KR20230106533A (en) | 2023-07-13 |

Family

ID=87160298

Family Applications (2)

| Application Number | Title | Priority Date | Filing Date |

|---|---|---|---|

| KR1020230068756APendingKR20230106533A (en) | 2023-05-27 | 2023-05-27 | Method and application for easy payment in mart |

| KR1020230104605ACeasedKR20240170748A (en) | 2023-05-27 | 2023-08-10 | Method and application for easy payment |

Family Applications After (1)

| Application Number | Title | Priority Date | Filing Date |

|---|---|---|---|

| KR1020230104605ACeasedKR20240170748A (en) | 2023-05-27 | 2023-08-10 | Method and application for easy payment |

Country Status (2)

| Country | Link |

|---|---|

| KR (2) | KR20230106533A (en) |

| WO (1) | WO2024248316A1 (en) |

Cited By (1)

| Publication number | Priority date | Publication date | Assignee | Title |

|---|---|---|---|---|

| WO2024248316A1 (en)* | 2023-05-27 | 2024-12-05 | 구도영 | Simple payment method and application |

Family Cites Families (7)

| Publication number | Priority date | Publication date | Assignee | Title |

|---|---|---|---|---|

| KR101934293B1 (en)* | 2012-08-03 | 2019-01-02 | 엘지전자 주식회사 | Mobile terminal and nfc payment method thereof |

| KR102174437B1 (en)* | 2012-08-24 | 2020-11-04 | 삼성전자주식회사 | Apparatus and method for providing interaction information by using image on device display |

| KR20170033841A (en)* | 2017-03-17 | 2017-03-27 | 이제원 | Payment information send/receive device by bluetooth communication, method and program for payment bt mobile device |

| KR101942661B1 (en)* | 2017-09-25 | 2019-02-22 | 브이피 주식회사 | Payment method for selecting comunication mode of transportation fee by hce type and mobile terminal thereof |

| KR20190067588A (en)* | 2017-12-07 | 2019-06-17 | 엘지전자 주식회사 | Mobile terminal and method for controlling the sagme |

| KR102631448B1 (en)* | 2021-06-09 | 2024-01-30 | 주식회사 지오플랜 | Method And System for Providing Public Transport Payment by using UWB |

| KR20230106533A (en)* | 2023-05-27 | 2023-07-13 | 구도영 | Method and application for easy payment in mart |

- 2023

- 2023-05-27KRKR1020230068756Apatent/KR20230106533A/enactivePending

- 2023-08-10KRKR1020230104605Apatent/KR20240170748A/ennot_activeCeased

- 2024

- 2024-04-09WOPCT/KR2024/004777patent/WO2024248316A1/enactivePending

Cited By (1)

| Publication number | Priority date | Publication date | Assignee | Title |

|---|---|---|---|---|

| WO2024248316A1 (en)* | 2023-05-27 | 2024-12-05 | 구도영 | Simple payment method and application |

Also Published As

| Publication number | Publication date |

|---|---|

| WO2024248316A1 (en) | 2024-12-05 |

| KR20240170748A (en) | 2024-12-04 |

Similar Documents

| Publication | Publication Date | Title |

|---|---|---|

| US11232438B2 (en) | Method and system for authenticating transaction request from device | |

| US10032157B2 (en) | Mobile device with disabling feature | |

| EP3458916B1 (en) | Authentication with smartwatch | |

| US9038894B2 (en) | Payment or other transaction through mobile device using NFC to access a contactless transaction card | |

| US10614465B2 (en) | Dynamic modification of a verification method associated with a transaction card | |

| US20170221043A1 (en) | Transaction facilitation methods and apparatuses | |

| US20130060701A1 (en) | Electronic payment service method, and electronic payment service apparatus, mobile communication terminal, and transaction terminal for performing the method | |

| US20080172340A1 (en) | Method and system for carrying out a transaction between a mobile device and a terminal | |

| KR101330670B1 (en) | Method and server for payment | |

| KR20130089896A (en) | Portable device, payment device, payment agency server having dutch pay function, and payment method and agency method for payment | |

| AU2014323499A1 (en) | Systems and methods for managing mobile account holder verification methods | |

| KR20110068116A (en) | Mobile terminal, smart card, and method for providing payment information | |

| US10742662B2 (en) | Non-transaction enabling data security | |

| KR20230106533A (en) | Method and application for easy payment in mart | |

| KR20120020804A (en) | Method and system of payment, and mobile terminal thereof | |

| AU2015358442B2 (en) | Methods and apparatus for conducting secure magnetic stripe card transactions with a proximity payment device | |

| KR20130132252A (en) | Mobile card payment system using near field communication, mobile communication terminal having mobile card payment function and the method thereof | |

| TW201401199A (en) | Trading method and mobile device performing the trading method | |

| KR20140081213A (en) | System for charging electronic card and method thereof | |

| TWM622036U (en) | Discount payment plan recommendation system | |

| KR20160047904A (en) | Method for indirectly payment through proximity sensing between the mobile terminal and server for the same | |

| CN120181847A (en) | A member payment method, device, equipment and medium | |

| HK1263173A1 (en) | Authentication with smartwatch | |

| KR20160081547A (en) | Payment Systems | |

| KR20140141209A (en) | A payment method using rf card and payment server |

Legal Events

| Date | Code | Title | Description |

|---|---|---|---|

| PA0109 | Patent application | Patent event code:PA01091R01D Comment text:Patent Application Patent event date:20230527 | |

| G15R | Request for early publication | ||

| PG1501 | Laying open of application | Comment text:Request for Early Opening Patent event code:PG15011R01I Patent event date:20230626 | |

| PC1204 | Withdrawal of earlier application forming a basis of a priority claim |