JP2006127174A - Personal authentication system for credit card payment - Google Patents

Personal authentication system for credit card paymentDownload PDFInfo

- Publication number

- JP2006127174A JP2006127174AJP2004314993AJP2004314993AJP2006127174AJP 2006127174 AJP2006127174 AJP 2006127174AJP 2004314993 AJP2004314993 AJP 2004314993AJP 2004314993 AJP2004314993 AJP 2004314993AJP 2006127174 AJP2006127174 AJP 2006127174A

- Authority

- JP

- Japan

- Prior art keywords

- settlement

- approval

- credit

- payment

- conditions

- Prior art date

- Legal status (The legal status is an assumption and is not a legal conclusion. Google has not performed a legal analysis and makes no representation as to the accuracy of the status listed.)

- Pending

Links

Images

Landscapes

- Financial Or Insurance-Related Operations Such As Payment And Settlement (AREA)

Abstract

Translated fromJapaneseDescription

Translated fromJapanese 本発明はクレジット決済承認を管理するシステムに係わり、特にクレジット決済利用者

が個人別に個人認証(サイン、生体認証等)無し決済の許可有無等の決済承認条件を事前

に登録することを実現する決済システム、また事前登録条件に反する決済に対し回避手段

を持ち決済を実現する決済システムに関する。The present invention relates to a system for managing credit settlement approval, and in particular, a settlement that realizes that a credit settlement user registers in advance settlement approval conditions such as permission / non-permission of settlement without individual authentication (signature, biometric authentication, etc.) for each individual. The present invention also relates to a payment system that has a means for avoiding payment that violates pre-registration conditions and realizes payment.

従来のクレジット決済システムは利用者情報としてクレジット種別、クレジットカード

番号、クレジット有効期限、クレジット決済上限金額等のカード情報の確認により決済を

承認している。実存する店舗における決済承認においてはサイン等の個人認証を店舗側で

行っているが、インターネットショッピング等のネット上および電話等における決済につ

いては上記クレジットカード情報のみの確認で、サイン等個人認証無しに決済認証が行わ

れる。このためセキュリティ上で問題があった。従来の技術として特開2004-110352号、

特開2003-30559号公報があげられるが、前者は事前に使用条件を登録するが複数クレジッ

トカードを1枚に統合し決済の種類によりどのクレジット会社を使用するかを自動で選択

し使い勝手向上を目的としたものであり、セキュリティレベルは現状通りである。後者は

本人承認のためクレジットカード会社がカード所有者の携帯電話(事前登録)に連絡し、認

証を実現するシステムでありセキュリティは向上するが、携帯電話不携帯の場合や決済承

認をバッチ処理で行うインターネットショッピング等では決済依頼時点より遅れて携帯電

話に承認依頼が来ることになり使い勝手に問題がある。A conventional credit settlement system approves settlement by checking card information such as a credit type, a credit card number, a credit expiration date, and a credit settlement upper limit amount as user information. Personal authentication such as signatures is performed at the store side for payment approval at existing stores, but for payments over the Internet, such as Internet shopping, etc., only confirmation of the above credit card information is required, and there is no personal authentication such as signatures Payment authentication is performed. For this reason, there was a problem in security. JP-A-2004-110352 as a conventional technique,

Japanese Patent Laid-Open No. 2003-30559 can be mentioned, but the former registers usage conditions in advance, but integrates multiple credit cards into one and automatically selects which credit company to use depending on the type of payment, improving usability It is intended and the security level is as it is. The latter is a system in which the credit card company contacts the cardholder's mobile phone (pre-registration) for authorization, and authentication is improved.Security is improved, but if the mobile phone is not mobile or payment approval is batch processed In Internet shopping or the like, there is a problem in usability because an approval request comes to the mobile phone after the settlement request time.

従来のクレジット決済システムでは、個人認証無しでも決済承認が完了するシステムの

ためセキュリティに問題がある。また特開2003-30559号公報にあげられるようにクレジッ

ト決済に個人認証を必須とし、決済時の携帯電話連絡による承認実施方法では、インター

ネットショッピング等の店舗側が決済処理をバッチで行う業態で利用する場合予期してい

ない時間に携帯電話承認を受けることになり使い勝手に問題がある。The conventional credit settlement system has a security problem because the settlement approval is completed without personal authentication. Also, as disclosed in Japanese Patent Application Laid-Open No. 2003-30559, personal authentication is essential for credit settlement, and in the method of performing approval by mobile phone contact at the time of settlement, the store side such as Internet shopping is used in a business mode in which settlement processing is performed in batches. In some cases, mobile phone approval is received at an unexpected time, which is a problem in usability.

本発明の目的は、上記課題を解決し、カード所有者の使い勝手を損なうことなくセキュ

リティを向上させたクレジット決済における個人認証システムを提供することにある。An object of the present invention is to provide a personal authentication system in credit settlement which solves the above-described problems and improves security without impairing the usability of the cardholder.

上記目的を達成するために、本発明はクレジット決済の認証を行うセンタにおいて個人

別の決済承認条件(個人認証無しでの承認有無、決済範囲、条件外決済発生時の承認手段

等)を事前に登録できる手段を備え、店舗からクレジット決済依頼を受信した際、クレジ

ット決済利用者個人の決済承認条件を検索する手段を備え、登録決済承認条件と不一致の

決済発生の場合には個人が事前登録した承認方法で承認確認を行う手段を備え、その確認

結果により決済処理を承認または拒否することを可能としたシステムである。In order to achieve the above-mentioned object, the present invention preliminarily sets individual payment approval conditions (whether approval is required without personal authentication, payment range, approval means when an out-of-condition payment occurs) in the center that performs credit payment authentication. It has a means to register, and when it receives a credit payment request from a store, it has a means to search for the payment approval condition of the individual user of credit payment, and the individual registered in advance if payment does not match the registered payment approval condition This is a system that includes a means for confirming approval by an approval method, and can approve or reject the settlement process based on the confirmation result.

かかる構成により、カード所有者が意図しない決済を承認せず、また決済承認条件不一

致の場合のカード所有者が事前登録した回避方法で承認処理が可能となる。With this configuration, the cardholder does not approve payment that is not intended, and approval processing can be performed by an avoidance method pre-registered by the cardholder when the payment approval conditions do not match.

本発明によれば、クレジット決済の利便性を損なうことなくセキュリティを向上させる

ことが可能となる。According to the present invention, security can be improved without impairing the convenience of credit settlement.

以下、図1〜図3を用いて、本発明の一実施形態によるシステムの構成について説明す

る。Hereinafter, the configuration of a system according to an embodiment of the present invention will be described with reference to FIGS.

最初に図1を用いて、本実施形態によるクレジット決済センタのシステム構成について

説明する。First, the system configuration of the credit settlement center according to the present embodiment will be described with reference to FIG.

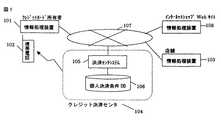

図1は本発明の一実施形態によるクレジットカード所有者の情報処理端末および携帯電

話、決済する店舗の情報処理装置、クレジット決済センタのシステム構成を示すブロック

図である。FIG. 1 is a block diagram showing the system configuration of an information processing terminal and a mobile phone of a credit card owner, an information processing device of a store for settlement, and a credit settlement center according to an embodiment of the present invention.

クレジットカード所有者(情報処理装置)101はインターネット107を介してイン

ターネットショップサイト情報処理装置108に接続されている。またインターネットシ

ョップサイト情報処理装置108および実在店舗の情報処理装置103はインターネット

107を介してクレジット決済センタ104の決済センタシステム105に接続されてい

る。決済センタシステム105はクレジットカード所有者の個人別決済条件の情報データ

ベースである個人決済条件DB106を備える。The credit card owner (information processing apparatus) 101 is connected to the Internet shop site

クレジット決済センタシステム105ではあらかじめクレジットカード所有者の決済条

件を個人決済条件DB106に持つ。In the credit

図2はクレジットカード所有者が事前に登録する決済条件を情報として蓄える個人決済

情報DB106の内容を示す。データベースの項目としては、カード所有者の特定のため

の「氏名」201、「カード番号」202を持つ。またサイン、生体認証等の個人認証無

し決済の許可有無を示す「個人認証無し決済」203を持ち、この「個人認証無し決済」

203が「OK」203−1の所有者「AAA」場合、個人認証無しの決済を許可するこ

とになり、許可範囲として「許可業種」204と許可上限金額「上限金額」205を設定

可能とする。所有者「AAA」201−1の場合、サイン等の個人認証無し決済を許可し

ている業種は「インターネット販売/テレホンショッピング」204−1のみであり、実

存する「店舗」204−2や「航空券」204−3等のその他の業種では許可しない設定

となり、また「上限金額」は「xxx」205−1と設定されている。所有者「BBB」

201−2の場合、サイン等の個人認証無し決済については「NG」203−2で許可し

ないことになり、「許可業種」204の設定は不可「−」204−4となる。FIG. 2 shows the contents of the personal

If the

In the case of 201-2, “NG” 203-2 does not permit settlement without personal authentication such as a signature, and “allowed industry” 204 cannot be set “−” 204-4.

またサイン等の「個人認証無し決済」203の許可如何に関わらず、設定条件203,

204および205と条件不一致の決済依頼が発生した場合の承認回避方法の設定有無を

示す「条件外承認」206がある。所有者「AAA」201−1の場合、条件外決済が発

生した場合「OK」206−1より回避方法による承認を行うことになる。「承認方法」

207に設定された「Tel aaa-bbb」207−1の内容に従い携帯電話への承認確認を実

施する。この際「通知時間帯」208の「10:00−17:00」208−1内容に従い登録さ

れた時間帯に承認確認が実施される。決済発生がこの時間帯でなければ、その時間帯にな

るまで承認確認処理が延期されることになる。承認結果により承認されれば決済は完了、

却下されれば決済不成立となる。所有者「BBB」201−2において条件外決済が発生

した場合は、「NG」206−2により条件外決済承認が許可されておらず決済不成立と

なる。Regardless of whether or not “payment without personal authentication” 203 such as a signature is permitted,

There is an “unconditional approval” 206 indicating whether or not an approval avoidance method is set when a settlement request that does not match the conditions of 204 and 205 is generated. In the case of the owner “AAA” 201-1, when an unconditional settlement occurs, the approval is made by the avoidance method from “OK” 206-1. "Approval Method"

In accordance with the contents of “Tel aaa-bbb” 207-1 set in 207, confirmation of approval to the mobile phone is performed. At this time, the approval confirmation is performed in the registered time zone according to the contents of “10: 00-17: 00” 208-1 of the “notification time zone” 208. If payment does not occur during this time period, the approval confirmation process will be postponed until that time period. If approved by the approval result, payment is completed,

If rejected, settlement will not be established. When an unconditional settlement occurs in the owner “BBB” 201-2, the unconditional settlement approval is not permitted by the “NG” 206-2 and the settlement is not established.

次に図3A及びBを用いて、本発明のクレジット決済の個人認証処理について説明する

。図3A及びBは本発明の処理および方法を示すフロー図である。Next, the personal authentication processing for credit settlement according to the present invention will be described with reference to FIGS. 3A and B are flow diagrams illustrating the process and method of the present invention.

所有者「AAA」がインターネットショップで23:00にクレジットカード決済を利用す

る場合を例にとって説明する。The case where the owner “AAA” uses credit card payment at 23:00 at an internet shop will be described as an example.

所有者「AAA」がWeb上のインターネットサイトで購入金額支払いをクレジット決

済とする為、クレジットカード種別/クレジットカード番号等必要情報を入力し(301

)、インターネットサイトへ送信する(302)。インターネットショップ側では送信さ

れたクレジットカード情報および購入内容を受信し(311)、クレジットカード情報と

決済金額および店舗情報として店名を識別する情報に加え業態を示すインターネットショ

ップである情報と個人認証なし決済であることを決済センタ(104)へ送信する(32

1)。ただし、Webサイトでのクレジット決済の場合、決済発生即時に決済センタへ決

済承認依頼がされるわけではなく、バッチ処理される場合が多い。このサイトがAM01

:00にバッチ処理にて決済センタへ承認依頼を行うと仮定して以降の処理を説明する。

決済センタでは受信したクレジットカード情報を個人決済条件DB(106、320)と

照合する(321)。まずクレジットカード種別・カード番号をDBの「カード番号」(

202)と照合しカード情報の有効性を判定する(322)。無効の場合、依頼元のイン

ターネットショップ側へ決済拒否の通知をする(322−1)。インターネットショップ

では拒否の通知を受信すると(313)、所有者「AAA」へクレジット決済が不成立で

あった通知を行う(303)。The owner “AAA” inputs necessary information such as the credit card type / credit card number in order to make the payment of the purchase amount credit payment on the Internet site on the Web (301

) To the Internet site (302). The Internet shop side receives the transmitted credit card information and purchase contents (311), and in addition to the information identifying the store name as the credit card information, the settlement amount and the store information, the information indicating the business type and the settlement without personal authentication To the settlement center (104) (32)

1). However, in the case of credit settlement at a Web site, a settlement approval request is not always made to the settlement center immediately after the settlement occurs, and batch processing is often performed. This site is AM01

Assuming that an approval request is made to the settlement center by batch processing at 0:00, the subsequent processing will be described.

The settlement center collates the received credit card information with the personal settlement condition DB (106, 320) (321). First, the credit card type and card number are stored in the “Card Number” (

202) and the validity of the card information is determined (322). If it is invalid, a settlement refusal notification is sent to the requesting Internet shop (322-1). When the Internet shop receives the refusal notice (313), it notifies the owner “AAA” that the credit settlement has not been established (303).

また、クレジットカード情報が有効の場合、インターネットショップから送信された情

報が「個人認証無し」であるため、DBを参照し「個人認証無し決済」(203)を許可

するかどうかを判定する(323)。所有者「AAA」の事前登録は「OK」(203−

1)で許可となっているので、次に決済条件の確認(324)処理を行う。ここではDB

より「AAA」の「許可業種」(204)を参照する。この場合該当する「インターネッ

ト販売 ○」(204−1)で許可設定、上限金額「xxx」(205−1)となってお

り、本決済が上限金額「xxx」を超えていなければ条件一致となり決済承認されインタ

ーネットショップへその旨が通知される(325−1,314)。「AAA」の場合、実

存する「店舗」(204−2)や「航空券」(204−3)等の「×」(204−2,2

04−3)に該当する業種からの決済依頼は個人認証無し決済が許可されていないので条

件不一致となる。条件不一致の場合、DBの「条件外承認」(206)を参照する。「A

AA」の場合、条件外の承認が「OK」(206−1)で許可されており、条件外発生時

の「承認方法」(207)が「Tel aaa-bbb」(207−1)と設定されている。従

って次に通知時間帯かどうかを判定する(327)。DBの「通知時間帯」(208)を

参照する。「AAA」の場合、「10:00−17:00」(208−1)となっており、AM1

:00は時間帯ではない為、通知開始時間になるまで待つことになる(327−1)。通

知時間帯になると登録された携帯電話の番号へ連絡することで承認確認を行う(328)

。ここで個人承認が得られれば決済承認(3210)となり、インターネットショップへ

承認通知を行う(3210−1)。個人承認が得られない場合はインターネットショップ

へ決済不成立の通知を行う(329−1)。If the credit card information is valid, the information transmitted from the Internet shop is “no personal authentication”, so it is determined whether or not “settlement without personal authentication” (203) is permitted by referring to the DB (323). ). Pre-registration of the owner “AAA” is “OK” (203−

Since it is permitted in 1), the settlement condition confirmation (324) processing is performed next. Here DB

Then, refer to “permitted industry” (204) of “AAA”. In this case, the corresponding “Internet sales ○” (204-1) is permitted, and the upper limit amount “xxx” (205-1). If this payment does not exceed the upper limit amount “xxx”, the condition is met and the payment is made. It is approved and notified to the Internet shop (325-1, 314). In the case of “AAA”, “x” (204-2, 2) such as an existing “store” (204-2) and “air ticket” (204-3).

The settlement request from the industry corresponding to 04-3) does not satisfy the condition because the settlement without personal authentication is not permitted. If the conditions do not match, refer to “unconditional approval” (206) in the DB. "A

In the case of “AA”, the approval outside the condition is permitted by “OK” (206-1), and the “approval method” (207) at the occurrence of the condition other than “Tel aaa-bbb” (207-1) is set. Has been. Therefore, it is next determined whether or not it is a notification time zone (327). Refer to “Notification Time Zone” (208) of DB. In the case of “AAA”, it is “10: 00-17: 00” (208-1), and AM1

Since 0:00 is not a time zone, it waits until the notification start time (327-1). Confirmation is confirmed by contacting the registered mobile phone number when the notification time comes (328)

. If personal approval is obtained here, settlement approval (3210) is made, and an approval notification is sent to the Internet shop (3210-1). If personal approval is not obtained, a notification that payment is not established is sent to the Internet shop (329-1).

次に所有者「BBB」がインターネットショップでクレジットカード決済を行う場合を

例にとって説明する。Next, the case where the owner “BBB” makes a credit card payment at an Internet shop will be described as an example.

所有者「BBB」がWeb上のインターネットサイトで購入金額支払いをクレジット決

済とするためクレジットカード種別/クレジットカード番号等必要情報を入力し(301

)、インターネットサイトへ送信する(302)。インタネットショップでは所有者「AA

A」利用の前記内容と同様にクレジット決済センタへ承認依頼を行う(312)。決済セ

ンタでも所有者「AAA」利用の前記内容と同様にDBとの照合により(321)、クレ

ジットカードの有効性を判断する(322)。有効性が確認されると決済が個人認証有り

なのかどうかが判定される(323)。ここではインターネットショップから送信された

情報が「個人認証無し」であるため、DBを参照し所有者「BBB」の登録内容を検索す

る。所有者「BBB」の事前登録は「NG」(203−2)で不許可となっているため、

登録内容と不一致の決済依頼が発生したと判断され(325)、不一致時の承認方法をD

Bより検索する(326)。「BBB」の「条件外承認」(206)は「NG」(206

−2)であり条件外の決済承認を拒否する内容となっている。このため決済は拒否されそ

の旨がインターネットショップへ通知される(326−1,315)。この通知を受けた

インターネットショップは所有者「BBB」に対するクレジット決済が不成立であったこ

とを通知する(303)。The owner “BBB” inputs necessary information such as the credit card type / credit card number in order to make the payment of the purchase amount credit payment on the Internet site on the Web (301

) To the Internet site (302). The owner “AA”

An approval request is made to the credit settlement center in the same manner as the above-mentioned content of “A” use (312). The settlement center also determines the validity of the credit card (322) by collating with the DB (321) in the same manner as in the case of using the owner "AAA" (322). If the validity is confirmed, it is determined whether or not the settlement has personal authentication (323). Here, since the information transmitted from the Internet shop is “no personal authentication”, the registered content of the owner “BBB” is searched with reference to the DB. Pre-registration of owner “BBB” is disapproved by “NG” (203-2).

It is determined that a settlement request that does not match the registered content has occurred (325), and the approval method for the mismatch is D

Search from B (326). “Non-conditional approval” (206) of “BBB” is “NG” (206

-2), and it is a content that rejects payment approval outside the conditions. For this reason, the settlement is rejected, and the fact is notified to the Internet shop (326-1, 315). Upon receiving this notification, the Internet shop notifies that the credit settlement for the owner “BBB” has not been established (303).

また、実存する店舗側等でサイン等による個人認証を行う決済については店舗側から送

信された情報に「個人認証有り」が含まれる。このため決済センタ側の個人認証無し決済

かどうかの判断(323)において、個人認証有り決済であるとされ決済承認される(3

14)。In addition, for payment that performs personal authentication using a signature or the like at an existing store side or the like, “with personal authentication” is included in the information transmitted from the store side. For this reason, in the determination (323) on the settlement center side whether the settlement is without personal authentication, it is determined that the settlement is with personal authentication and the settlement is approved (3

14).

以上説明したように、本実施形態のよればクレジットカード所有者毎に決済条件、特に

個人認証無し決済の許可についての有無/許可の場合の決済可能範囲を事前登録すること

によってセキュリティを向上させることが可能となる。また、条件外の決済が発生した際

の回避策として携帯電話への連絡による承認手段を所有者の希望により設定することがで

きる。これによりクレジット決済の利便性を損なうことなくセキュリティを向上させるこ

とが可能となる。As described above, according to the present embodiment, the security is improved by pre-registering the settlement conditions for each credit card holder, in particular, the settlement range in the presence / absence of permission for settlement without personal authentication. Is possible. In addition, as an avoidance measure when an unsettled settlement occurs, an approval means by contacting a mobile phone can be set according to the desire of the owner. This makes it possible to improve security without impairing the convenience of credit settlement.

101…情報処理装置、102…携帯電話、103…店舗側情報処理装置、104…ク

レジット決済センタ、105…決済センタシステム、106…個人決済条件データベース

、107…ネットワーク、108…インターネットショップWebサイト側情報処理装置

、200…決済センタ(個人決済条件データベース)、320…決済センタ(個人決済条

件データベース)。

DESCRIPTION OF

Claims (3)

Translated fromJapanese無しでの承認有無、承認有りの場合の決済範囲等)を事前に登録できる手段を備え、店舗

からクレジット決済依頼を受信した際、クレジット決済利用者個人の決済承認条件を検索

する手段を備え、登録決済承認条件と不一致の決済発生の場合には個人が事前登録した承

認手段で承認確認を行う手段を備え、その確認結果により決済処理を承認または拒否する

ことを特徴とするクレジット決済システム。A credit settlement request is received from the store with means to register in advance payment approval conditions for each individual at the credit card authentication center (presence of approval without personal authentication such as signature, settlement range when there is approval, etc.) If the payment settlement condition does not match the registered settlement approval conditions, the credit settlement user has a means to check the approval with the pre-registered approval means. A credit settlement system, which approves or rejects settlement processing according to a result.

サイン、生体認証等)無しの決済許可の有無、許可有りの場合の範囲条件(店舗業態、業

種、上限金額等)を事前登録することを可能としたクレジット決済システム。In the credit settlement system according to claim 1, personal authentication (

A credit payment system that enables pre-registration of whether or not payment is permitted without signatures, biometrics, etc., and the range conditions (store business type, industry, upper limit, etc.) when permission is granted.

した場合、決済センタは個人が事前登録した承認方法による個人承認を得るまで決済を承

認しないことを可能とするクレジット決済システム。

3. The credit settlement system according to claim 1, wherein when a settlement that does not match the settlement conditions for each individual occurs, the settlement center can not approve the settlement until the individual obtains the personal approval by the pre-registered approval method. system.

Priority Applications (1)

| Application Number | Priority Date | Filing Date | Title |

|---|---|---|---|

| JP2004314993AJP2006127174A (en) | 2004-10-29 | 2004-10-29 | Personal authentication system for credit card payment |

Applications Claiming Priority (1)

| Application Number | Priority Date | Filing Date | Title |

|---|---|---|---|

| JP2004314993AJP2006127174A (en) | 2004-10-29 | 2004-10-29 | Personal authentication system for credit card payment |

Publications (1)

| Publication Number | Publication Date |

|---|---|

| JP2006127174Atrue JP2006127174A (en) | 2006-05-18 |

Family

ID=36721876

Family Applications (1)

| Application Number | Title | Priority Date | Filing Date |

|---|---|---|---|

| JP2004314993APendingJP2006127174A (en) | 2004-10-29 | 2004-10-29 | Personal authentication system for credit card payment |

Country Status (1)

| Country | Link |

|---|---|

| JP (1) | JP2006127174A (en) |

Cited By (9)

| Publication number | Priority date | Publication date | Assignee | Title |

|---|---|---|---|---|

| JP2007293713A (en)* | 2006-04-26 | 2007-11-08 | Fujitsu Fip Corp | Card management server, card management system, card management method, and card management program |

| JP2008176466A (en)* | 2007-01-17 | 2008-07-31 | Sumitomo Mitsui Card Co Ltd | Usage limit management device and IC chip |

| KR101274086B1 (en) | 2012-03-06 | 2013-06-17 | 인테그레이티드에너지 주식회사 | Smart card and storage media storing the same |

| JP2014522022A (en)* | 2011-06-27 | 2014-08-28 | アマゾン テクノロジーズ インコーポレイテッド | Payment selection and approval by mobile devices |

| JP2015062129A (en)* | 2010-05-14 | 2015-04-02 | オーセンティファイ・インクAuthentify Inc. | Flexible quasi-out-of-band authentication structure |

| WO2017019972A1 (en)* | 2015-07-30 | 2017-02-02 | Visa International Service Association | System and method for conducting transactions using biometric verification |

| US10055740B2 (en) | 2011-06-27 | 2018-08-21 | Amazon Technologies, Inc. | Payment selection and authorization |

| JP2020515935A (en)* | 2017-01-06 | 2020-05-28 | マスターカード インターナシヨナル インコーポレーテツド | IOT-compatible payment method and system |

| KR20230024437A (en)* | 2016-09-06 | 2023-02-20 | 애플 인크. | Express credential transaction system |

- 2004

- 2004-10-29JPJP2004314993Apatent/JP2006127174A/enactivePending

Cited By (12)

| Publication number | Priority date | Publication date | Assignee | Title |

|---|---|---|---|---|

| JP2007293713A (en)* | 2006-04-26 | 2007-11-08 | Fujitsu Fip Corp | Card management server, card management system, card management method, and card management program |

| JP2008176466A (en)* | 2007-01-17 | 2008-07-31 | Sumitomo Mitsui Card Co Ltd | Usage limit management device and IC chip |

| JP2015062129A (en)* | 2010-05-14 | 2015-04-02 | オーセンティファイ・インクAuthentify Inc. | Flexible quasi-out-of-band authentication structure |

| JP2014522022A (en)* | 2011-06-27 | 2014-08-28 | アマゾン テクノロジーズ インコーポレイテッド | Payment selection and approval by mobile devices |

| US10055740B2 (en) | 2011-06-27 | 2018-08-21 | Amazon Technologies, Inc. | Payment selection and authorization |

| KR101274086B1 (en) | 2012-03-06 | 2013-06-17 | 인테그레이티드에너지 주식회사 | Smart card and storage media storing the same |

| WO2017019972A1 (en)* | 2015-07-30 | 2017-02-02 | Visa International Service Association | System and method for conducting transactions using biometric verification |

| US10902103B2 (en) | 2015-07-30 | 2021-01-26 | Visa International Service Association | System and method for conducting transactions using biometric verification |

| US11609978B2 (en) | 2015-07-30 | 2023-03-21 | Visa International Service Association | System and method for conducting transaction using biometric verification |

| KR20230024437A (en)* | 2016-09-06 | 2023-02-20 | 애플 인크. | Express credential transaction system |

| KR102744827B1 (en)* | 2016-09-06 | 2024-12-19 | 애플 인크. | Express credential transaction system |

| JP2020515935A (en)* | 2017-01-06 | 2020-05-28 | マスターカード インターナシヨナル インコーポレーテツド | IOT-compatible payment method and system |

Similar Documents

| Publication | Publication Date | Title |

|---|---|---|

| AU2012202260B2 (en) | Methods and Systems for Conducting Payment Transactions | |

| AU2010256666B2 (en) | System and method for providing authentication for card not present transactions using mobile device | |

| AU2007234789B2 (en) | Methods and systems for enhanced consumer payment | |

| US11935058B2 (en) | Systems and methods for authenticating a user using private network credentials | |

| JP2002245243A (en) | Private and secure financial transaction system and method | |

| US20180247287A1 (en) | Methods and systems for performing a mobile-to-business anywhere ecommerce transaction using a mobile device | |

| US20110276486A1 (en) | System and method for securing payment | |

| JP2004310778A (en) | Credit transaction system and method using fingerprint information | |

| CN102792325A (en) | System and method for securely validating transactions | |

| RU2735398C2 (en) | System and method using time-reduced processing device | |

| US20200193514A1 (en) | Systems and Methods for Onsite or Remote Dispensing of Credit Instruments | |

| US20140289061A1 (en) | Point-of-sale terminal based mobile electronic wallet registration, authorization and settlement | |

| US20100161470A1 (en) | Systems and methods for authenticating an identity of a user of a transaction card | |

| US20140358704A1 (en) | Secured point-of-sale transactions | |

| US20170109663A1 (en) | Payment processing system for a providing a merchant with a prepaid card for use with a reservation | |

| JP2007241359A (en) | Automatic transaction system | |

| JP2006127174A (en) | Personal authentication system for credit card payment | |

| JP2002042034A (en) | Settlement determination apparatus and method, and settlement system using cash substitute | |

| JP2014032517A (en) | Settlement processing system, method, and computer program | |

| JP2003168063A (en) | Payment approval method and system in card payment method | |

| US10949857B2 (en) | Amount confirmation for visually impaired users | |

| JP2013246580A (en) | Credit examination system, credit examination method and in-store terminal | |

| JP2005182338A (en) | Credit card authentication system using mobile phone | |

| JP2003228683A (en) | Third party in credit settlement, control method of third party, program and recording medium | |

| JP2005275923A (en) | Individual authentication method at the time of card settlement, individual authentication system at the time of card settlement, shop information processing system, credit-card company information processing system, portable terminal, and program therefor |

Legal Events

| Date | Code | Title | Description |

|---|---|---|---|

| RD04 | Notification of resignation of power of attorney | Free format text:JAPANESE INTERMEDIATE CODE: A7424 Effective date:20060509 |